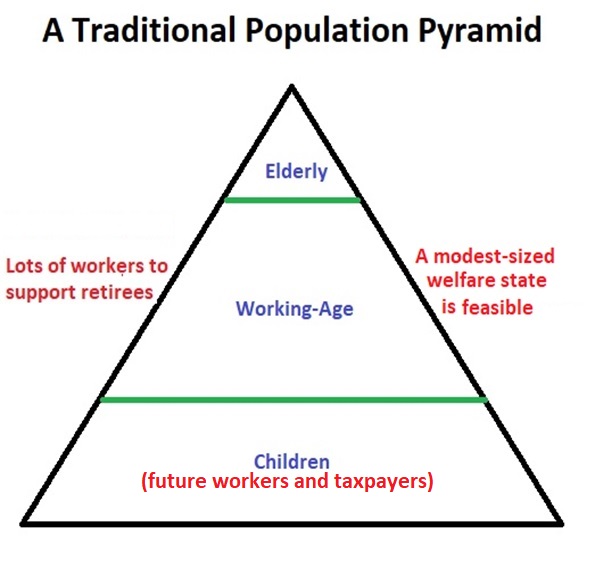

Let’s start today’s column with two simple and uncontroversial statements.

- Without real entitlement reform, the burden of government spending will grow dramatically over the next few decades.

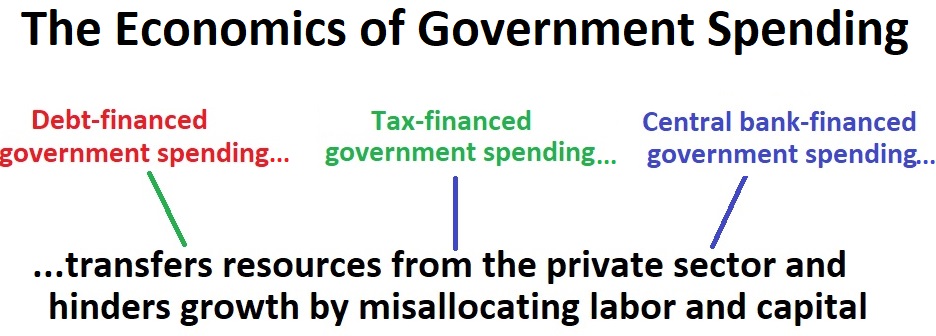

- There are only three ways – taxes, borrowing, and money-printing – to finance this rising burden burden of government.

Now I’ll add a statement that is controversial. As depicted by this visual I created in 2021, the productive sector of the economy is damaged regardless of how government is financed.

But it doesn’t matter whether you agree with me about the negative impact of big government. If government continues to grow rapidly, it will be financed by one of those three methods.

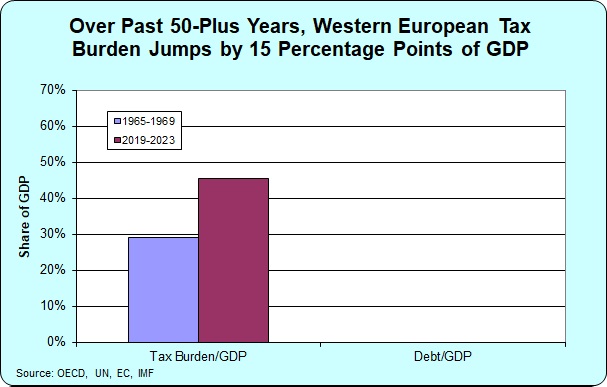

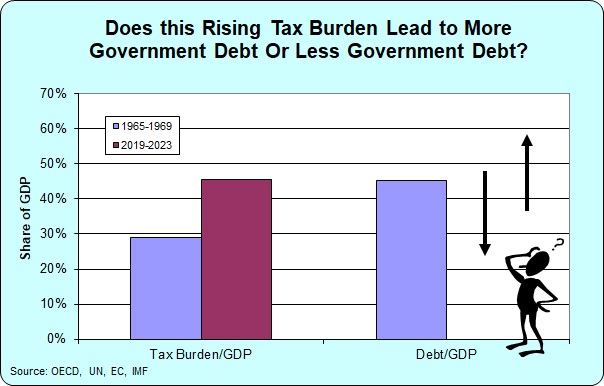

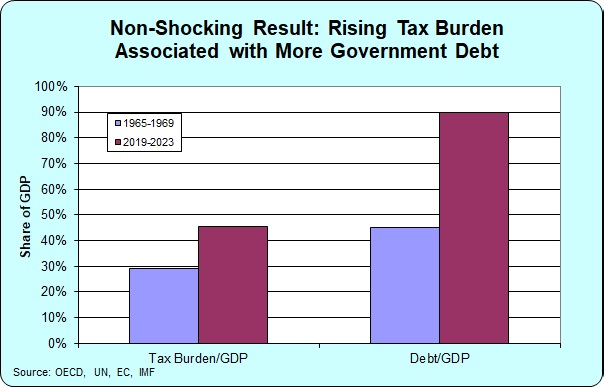

If you look at recent history, politicians have been paying for the rising burden of government with the first option – i.e., more red ink.

But this is not a stable long-run option, so I think that politicians sooner or later will opt for higher taxes, the middle option.

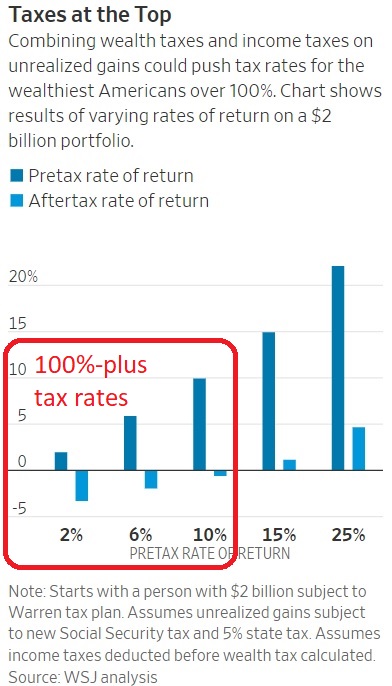

And since the rich already are being squeezed about as much as possible, the real long-run danger is much higher taxes on lower-income and middle-class Americans.

Which is exactly what happened in Europe (as noted by the 12th Theorem of Government).

However, perhaps I have not been sufficiently concerned about the third option. Veronique de Rugy has a new article in Reason about the risk that politicians will use the proverbial printing press to finance bigger government.

Here are some excerpts.

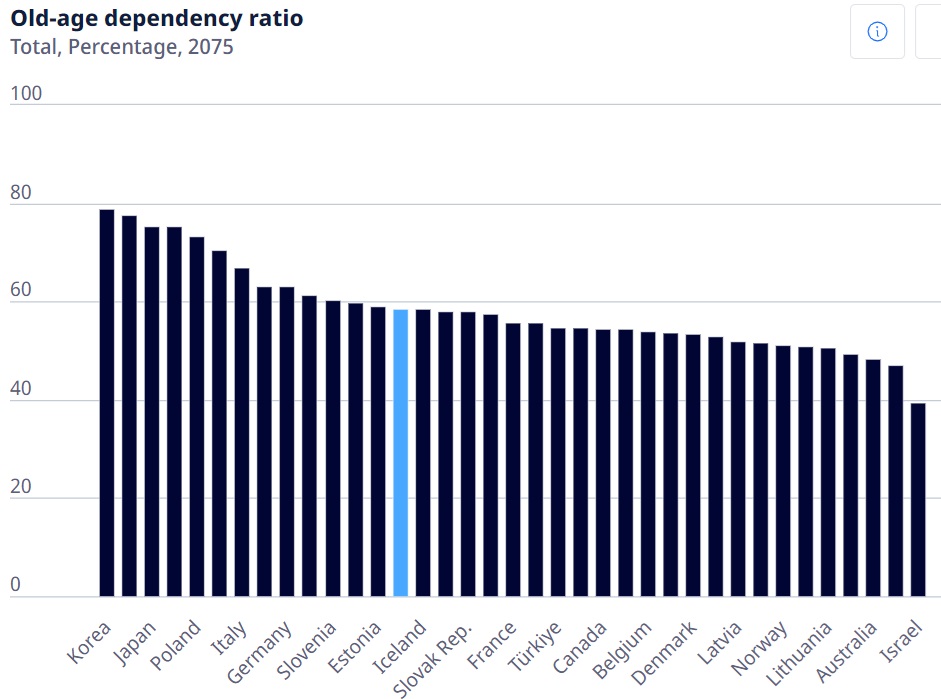

The easy, though irresponsible, political path may seem obvious: ..keep benefits whole, and pay by borrowing the money. This way legislators won’t have to cast unpopular votes… According to the Congressional Budget Office, borrowing to cover Social Security and Medicare shortfalls would push federal debt to about 156 percent of gross domestic product (GDP) by 2055. These shortfalls account for roughly $116 trillion, including interest, over those 30 years.

In spite of all this debt, the projections assume inflation stays low for decades and interest rates only go up very slowly. That calm outlook is misleading. …We saw this happen just a few years ago, between 2020 and 2022, when Congress approved about $5 trillion in debt-financed spending… Inflation followed… The entitlement deadline could trigger an even stronger reaction. Senators elected this year will be tempted to borrow everything needed to preserve benefits. …At that point, the Fed would be in a terrible position. …Inflation is a silent, unvoted-on tax. It eats away at savings, pensions, and fixed incomes. It hurts retirees… It squeezes workers whose paychecks don’t keep up with rising prices. It pushes families to spend more on groceries, rent, energy, and health care. And it distorts the entire economy by rewarding speculation over productive investment. No one escapes. Not the poor. Not the middle class. Not even the wealthy. It’s the most painful way to finance government promises.

Veronique’s column is persuasive.

Voters don’t like inflation, but they also don’t like higher taxes. This is why I’ve assumed politicians will opt for debt-financed spending.

But debt-financed spending only works until the “bond vigilantes” decide that a government is untrustworthy. And maybe politicians are nervous about reaching that point, in which case they’ll push for the money-printing option (monetary economists refer to this as “fiscal dominance“) in hopes of postponing such a debt crisis.

Since there’s no way of knowing how future politicians will behave, there’s no way to know for sure what will happen.

However, there is one thing we can say with certainty: Whether the final outcome is more debt, more taxes, or more inflation, something bad certainly will happen if politicians don’t limit the growing burden of government.

The bottom line is that we know how to define good fiscal policy. And we know the best way to handcuff politicians so that we can get good fiscal policy.

Unfortunately, we don’t know how to convince politicians to put on handcuffs when it interferes with their desire to buy votes.