This is why a recession will catalyze a collapse of the credit-asset bubble-dependent economy down to its foundations.

Narrative control works by having a pat answer for every skepticism and every doubt. Boiled down, the dominant narrative holds that the Federal Reserve (central banking) and the central government have the tools to quickly reverse any dip in GDP, a.k.a. recession, and return the economy to expansion.

The unstated foundation of this narrative is that recessions are bad, as only permanent expansion is good. That this isn't "free market capitalism" doesn't bother anyone, because the whole point of central banking and government is to eliminate the rough edges of "free market capitalism" with the sandpaper of "state capitalism," which creates or borrows as much money as needed to smooth over any spots of bother, a.k.a. recessions.

That recessions are essential market dynamics is not part of the narrative, which is conveniently binary: recessions bad, expansion good. Markets reflect human emotions, famously fear and greed, which manifest as debt and speculation, a.k.a. animal spirits: when we're confident and feeding off an expansion that appears to have no limit, then we borrow more money (debt expands) and "allocate the capital" (i.e. place it at risk to reap a future gain) to increasingly risky speculative investments.

This allocation of borrowed money into speculative assets pushes the price of those assets higher, increasing the collateral to support further borrowing to fund more speculation. In this manner, debt, asset valuations, collateral and speculation all fuel one another in a seemingly endless expansion that makes every participant richer.

This pyramiding of debt and "wealth" generates two self-liquidating dynamics: interest and risk. All debt comes with interest, the compensation due those who put their money at risk by lending it to the borrower. This debt service rises as debt expands, and also as risk increases: the riskier the speculation and the borrower, the higher the interest rate paid by the borrower.

Central banks can play games to reduce interest rates even as risk and interest payment rise, but since central banks own only a fraction of the total outstanding debt, their ability to "corner the market" is nil.

Their gaming the system to enable further expansion of debt and speculation functions not by actually buying up the majority of the new debt, it functions as a signal: the Federal Reserve has our back, they will bail out / recapitalize any lender losses while suppressing interest rates below what the unfettered market would demand, and so the pyramiding of debt, speculation and "wealth" can continue, apparently indefinitely.

But signaling has intrinsic limits, for it doesn't increase the income needed to service additional debt or guarantee speculations will pay off. These are the Achilles Heels of the central banking perpetual motion machine: for the vast majority of borrowers, both private and public, income doesn't automatically increase as debt increases. Income is influenced by market factors (supply and demand), technologies, state interventions (subsidies, stimulus spending, etc.) and the expansion or contraction of debt, interest rates and speculative investments.

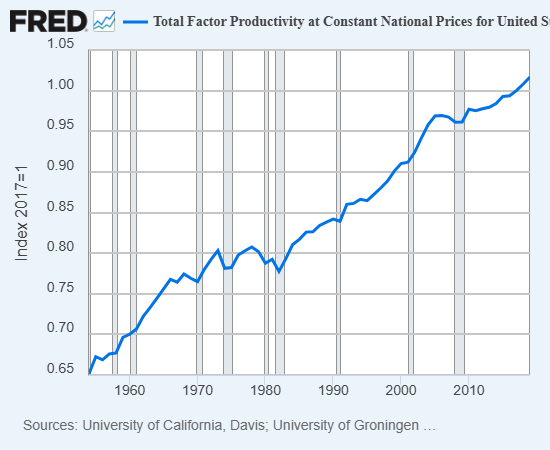

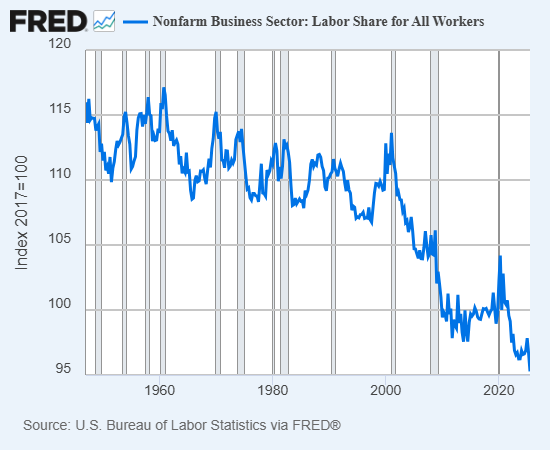

In the total-economy context, what matters are total factor productivity gains and the distribution of those gains to wage earners, enterprises, owners of assets and the state, which collects taxes from all three of the private-sector classes. This distribution changes with social, political and financial tides.

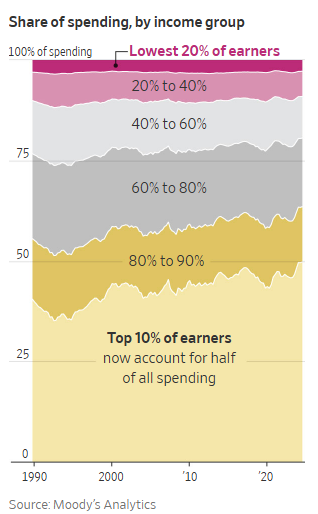

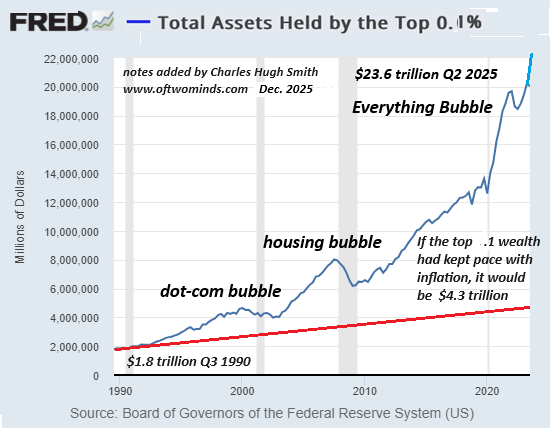

The past 50 years have seen productivity gains flow to capital (corporations and owners of assets) at the expense of wage-earners. This means households and small businesses must service debt from a shrinking share of the economy. As a result, borrowing more becomes increasingly risky for both borrower and lender.

As more of the output goes to corporations and owners of assets, their collateral, income and creditworthiness rise, meaning they can borrow more at lower rates of interest than wage earners and small enterprises. The more they can borrow, the more they can own and the more they can earn.

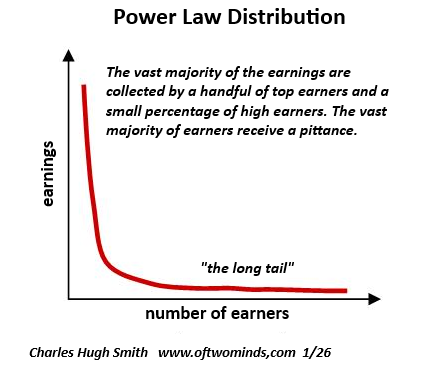

These are the core engines of extreme wealth and income inequality. The rich get richer because they have the means to borrow more income-generating assets at lower rates than wage earners. And unlike wages, this asset-generated income rises as assets increasing in value support additional borrowing as they serve as collateral.

On the most fundamental level, if economic expansion no longer increases the income of household borrowers enough to service more debt, the entire structure of expanding debt, collateral and speculation is destabilized. Ultimately, assets generate income from either 1) issuing more debt, 2) investing more in risk assets or 3) consumer spending. All three are interconnected, i.e. tightly bound, as any decline in the expansion of debt, investing or spending eventually bleeds through to reduced ability to service more debt and the end of the expansion of debt.

Since debt is inherently risky--borrowers can default, i.e. stop paying interest and principal on the debt--then depending on expanding debt for economic expansion is also increasing risk, especially if household earnings are stagnating while debt and interest payments are increasing.

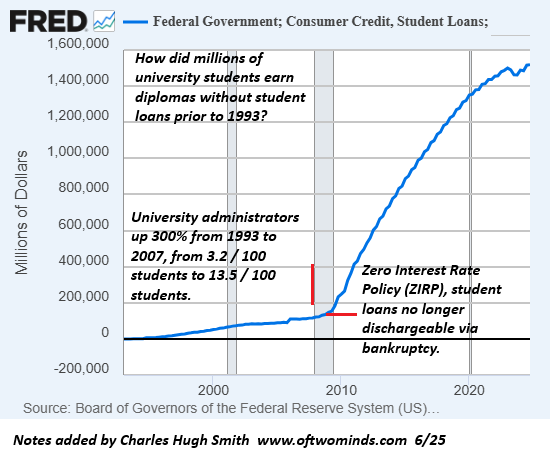

Since the percentage of output flowing to wages has been declining for 50 years, households have funded spending by borrowing more money. Prior to the 2000s, college students borrowed very little to fund their education. Now student loan debt is measured in the trillion-dollar range. Auto loans and credit card debt has also soared, along with shadow-banking debt that isn't even tracked: pay-in-installments, etc.

Speculative investments are also inherently risky: the investment can fail to pay off. If the speculation was funded by debt, then both the borrower and the lender go broke when the speculation fails.

Stagnating earnings, increasing debt to fund spending and increasingly risky debt-funded speculation generate a credit-asset bubble-dependent economy: economic expansion is now dependent on debt expanding to fund spending and the speculation that pushes asset valuations higher, increasing the collateral for even more borrowing.

Once income is no longer rising fast enough to service higher debt loads, defaults cascade throughout the system, triggering avalanches of declining income for both assets and wage earners as households default on rent, auto loans, student loans, credit cards and mortgages, collapsing consumer spending and laying waste to lenders and employers, who respond by reducing borrowing and laying off employees.

Speculations that looked sound in expansion go broke as lenders pull risky loans, household spending dries up and collateral collapses as risk assets are sold off to reduce risk by raising cash and paying down debt.

Credit-asset bubble-dependent economies are tightly bound systems: any drop in income and valuations, any tightening of credit, any rise in interest rates and any decline in collateral (i.e. the valuations of risk assets) feeds back into every other part of the system, creating a self-reinforcing feedback loop of defaults, layoffs and sagging asset valuations.

In an economy saturated with debt, stimulus doesn't generate expansion, it generates inflation which limits central bank stimulus. Without that signal that "the Fed has our back," speculation and the borrowing that funded it both dry up. Once the inflow of new credit-funded investment falters, asset valuations enter a self-reinforcing free-fall.

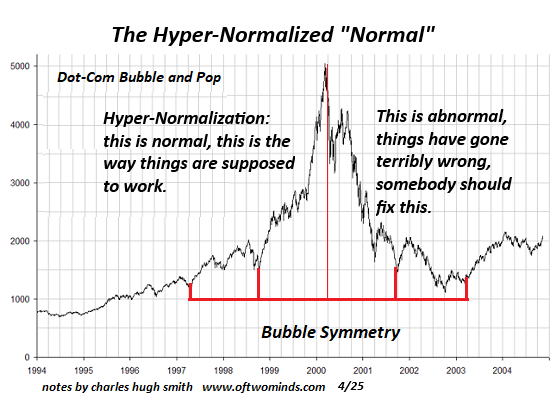

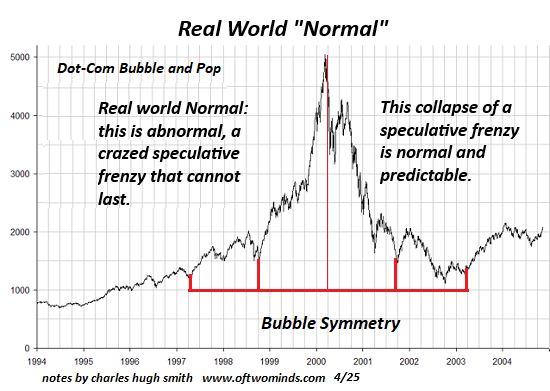

In a credit-asset bubble-dependent economy, this inevitable unwinding is viewed as an unexpected catastrophe:

In an economy that allowed recessions to clear bad debt and excessive speculation, credit-asset bubbles popping is viewed as inevitable and normal.

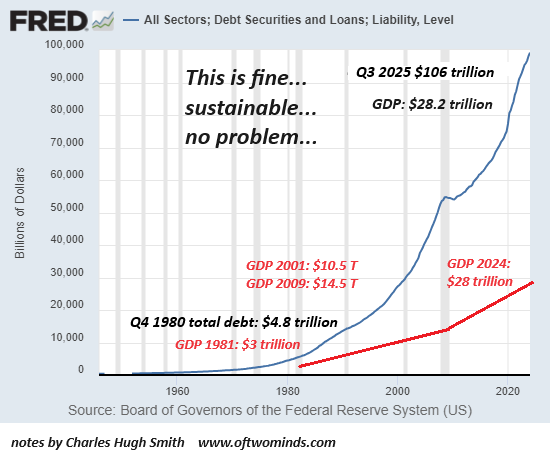

What few seem to understand is 1) the last "real recession" that cleared excesses of debt, leverage and speculation was 1980-82, 45 years ago and 2) the buffers that enabled the eventual recovery back then are gone. Where total debt was low in 1980--about 50% more than GDP--now it's triple GDP. That means "borrowing our way to expansion" isn't possible: borrowers are already unable to service existing debt, never mind more debt.

As for the Fed rescuing the debt bubble by dropping interest rates to zero: recall that the Fed isn't buying more than a sliver of the $106 trillion debt; it's only generating a false signal that risk is low. In the real world, risk is rising inexorably due to excessive debt, interest payments, leverage and speculation.

As for bailing the system out as in 2008, that is no longer possible, either. The system was "saved" by recapitalizing the financial sector--the source of new debt and speculation. But this time around, the economy is saturated with debt, income has stagnated and cannot support more borrowing, and the credit-asset bubbles in housing and financial assets has reached unprecedented heights of risk, i.e. fragility.

This is why a recession that clears the system of excessive debt, leverage and speculation leaves a devastated economy incapable of expansion: the system is now totally dependent on excesses of debt, leverage and speculation for its survival, never mind expansion, and once that collapses (as all bubbles do), the signaling, confidence and wealth that enabled the bubble will no longer exist.

As for saving the system by converting fiat money to precious metals or cryptocurrencies: the debt--and the income needed to service the debt--will also be converted, and that doesn't change the inevitable collapse of credit-asset bubbles and all the economic activity that depended on the permanent expansion of that credit-asset bubble.

This is why a recession will catalyze a collapse of the credit-asset bubble-dependent economy down to its foundations. A re-inflation of a new credit-asset bubble will be viewed as the "solution," but that unstable system will no longer be viable. The real solution will be re-arranging the economy to thrive not on credit-asset bubbles but on productivity gains that are widely distributed to all the productive elements, not just the wealthiest asset owners.

This process will be time-consuming and difficult, as all the "winners" in the current bubble economy will expect both a return to outsized gains and a continuation of their outsized share of the gains. Neither will be possible, as the changes will demand time, sacrifice and massive long-term investment in productive assets.

The systemic risks inherent to a credit-asset bubble-dependent economy cannot be extinguished, they can only be cloaked or transferred to others. These artifices enable the expansion of the bubble at a cost paid by everyone when the system's self-liquidating dynamics pop the bubble.

My new book Investing In Revolution is available at a 10% discount ($18 for the paperback, $24 for the hardcover and $8.95 for the ebook edition).

Introduction (free)

Check out my updated Books and Films.

Become

a $3/month patron of my work via patreon.com

Subscribe to my Substack for free

NOTE: Contributions/subscriptions are acknowledged in the order received. Your name and email

remain confidential and will not be given to any other individual, company or agency.

|

Thank you, David K. ($300), for your beyond outrageously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Jamshyd H. ($50), for your magnificently generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, John D. ($200) for your beyond outrageously generous subscription

to this site -- I am greatly honored by your support and readership.

|

|

Thank you, Colin G. ($70) for your splendidly generous subscription

to this site -- I am greatly honored by your support and readership.

|

Read more...