-

FINGRAPH

-

Data Ingestion Flowchart

-

Architecture Diagram

-

Freelancer 1 Profile

-

Freelancer 2 Profile

Introduction

On October 31st, 2023, Bloomberg reported that independent contractors and freelancers are increasingly essential—yet still sidelined by traditional finance:

“Freelancer reliance rises in U.S., with 20% of corporate work now done by them.”

Source: Bloomberg

Despite earning steadily, many freelancers continue to be flagged as “high-risk” simply because their income does not resemble W-2 employment.

A 2022 McKinsey report reinforced the scale of this shift:

36% of U.S. employed adults—58 million people—identify as independent workers.

Source: McKinsey & Company

Yet nearly 49% of gig and 1099 workers have been denied financial services they could afford, largely due to irregular or unverifiable income.

Source: Business Wire

Freelancers are financially active but remain structurally invisible. Their money flows across clients, subscriptions, transfers, bills, and merchants—patterns that behave like a graph, not a paycheck.

Traditional credit systems flatten this richness into a single number.

FinGraph exists to address this gap.

Inspiration, Problem and Why FinGraph ?

The idea originated from hearing the same story repeated across design, consulting, gig work, and creator communities:

“My income is stable, but the system still rejects me.”

This happens because legacy credit models expect:

- Single-employer income

- Predictable pay cycles

- Low spending variability

- Traditional bills and obligations

Freelancers violate these assumptions. Their financial behavior includes:

- Multi-sourced, asynchronous income

- Irregular bills and subscriptions

- Client concentration risk

- Month-to-month cashflow shifts

The issue isn’t poor financial behavior—it’s a model built for an outdated workforce.

FinGraph evaluates freelancers based on real behavior, not rigid templates.

Instead of asking “How much did you make?”, FinGraph asks:

- How stable is your income?

- How diversified are your clients?

- Which subscriptions drive expenses?

- How volatile is your cashflow?

- How much savings runway do you have?

These are graph questions.

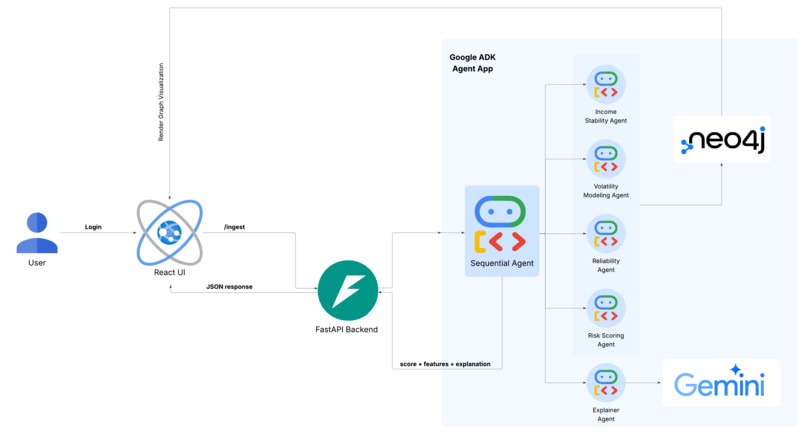

How it works ?

1. Data Layer — Real Banking Data

FinGraph reconstructs a freelancer’s financial world using the Capital One Nessie API

→ http://api.nessieisreal.com/

All data—accounts, deposits, withdrawals, transfers, merchants, and bills—is modeled as nodes and relationships inside Neo4j AuraDB.

2. Intelligence Layer — Multi-Agent Reasoning (ADK)

On top of the graph, FinGraph runs a structured multi-agent pipeline using Google’s Agent Development Kit (ADK). The agents are:

- Income Stability Agent – income cycles and irregularity

- Volatility Modeling Agent – cashflow variance and drawdowns

- Reliability Agent – client concentration, late payments, subscriptions

- Risk Scoring Agent – Financial Identity Score + savings runway

- Explainer Agent – grounded narrative from structured metrics

Agents communicate through JSON-based state passing, ensuring the reasoning remains grounded in real data and avoids hallucinations.

3. Application Layer — Dashboard

- Backend: Python + FastAPI + ADK

- Frontend: React + Neovis.js

- Deployment: Cloud Run

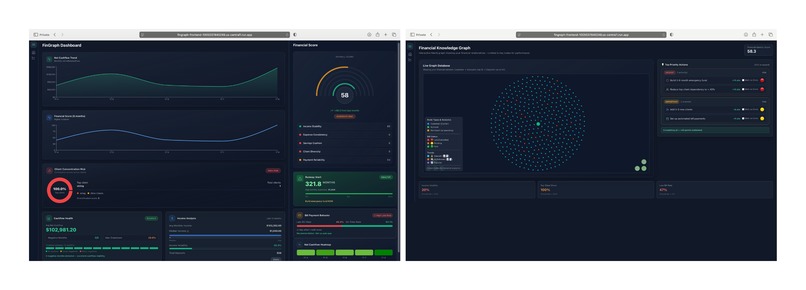

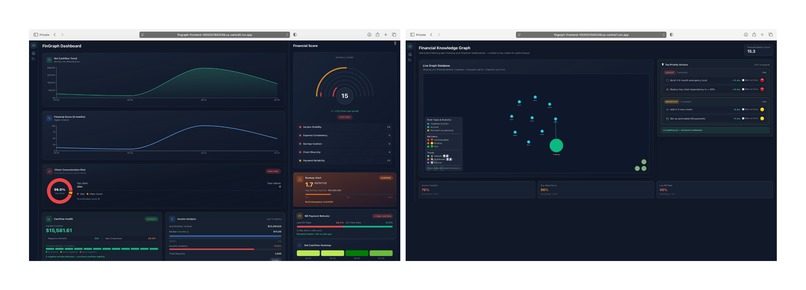

The dashboard presents:

- The Financial Identity Score

- Component breakdowns

- Timelines for income and cashflow

- Client concentration insights

- Savings runway

- An interactive Neo4j financial relationship graph

- Human-readable recommendations

Challenges we encountered

- Designing a unified graph schema from heterogeneous API data

- Writing precise Cypher queries to support our tools

- Constructing a multi-agent ADK pipeline with reliable state sharing

- Preventing LLM hallucinations

- Integrating ADK, Neo4j, FastAPI, and React cohesively

- Rendering large graph structures without overwhelming users

Every part required careful debugging and alignment across data, agents, and UI.

Conclusion

FinGraph reframes financial stability for a world increasingly powered by independent work. By combining graph databases, real banking data, and Gemini-powered multi-agent reasoning, it transforms fragmented transactions into a clear, human-centered Financial Identity. This isn’t a budgeting tool—it’s a new interpretation of financial identity itself, one that tells a story traditional credit scores never could.

Our approach naturally aligns with the goals of Technica, Intuit, Capital One, and MLH: we use AI responsibly, apply real financial data to solve an underserved problem, promote transparency and fairness, and build inclusive technology that empowers freelancers.

Accomplishments

- Fully working multi-agent reasoning pipeline

- Real financial graph from Nessie API ( ~87,000 accounts processed )

- Transparent scoring model

- Clean, fast dashboard ( < 4 seconds)

- Integrated explainability across all steps

What we learned

We learned to design graph-based financial models, orchestrate multi-agent LLM systems, generate grounded explanations, and build real-time analytics pipelines.

What's next for FinGraph

- Forecasting income and expenses

- Scenario simulation (“What if my top client leaves?”)

- Multi-bank support

- Personalized guidance beyond scoring

- Adaptive user insights

Testing Credentials

For evaluation and demonstration purposes, the following sample credentials have been provided.

Credential 1: Username: [email protected] Password: f20dd5184160

Credential 2: Username: electronic [email protected] Password: 35571461272f

Please note that these credentials are intended only for testing in a controlled environment and do not provide access to any production-level or sensitive information.

Log in or sign up for Devpost to join the conversation.