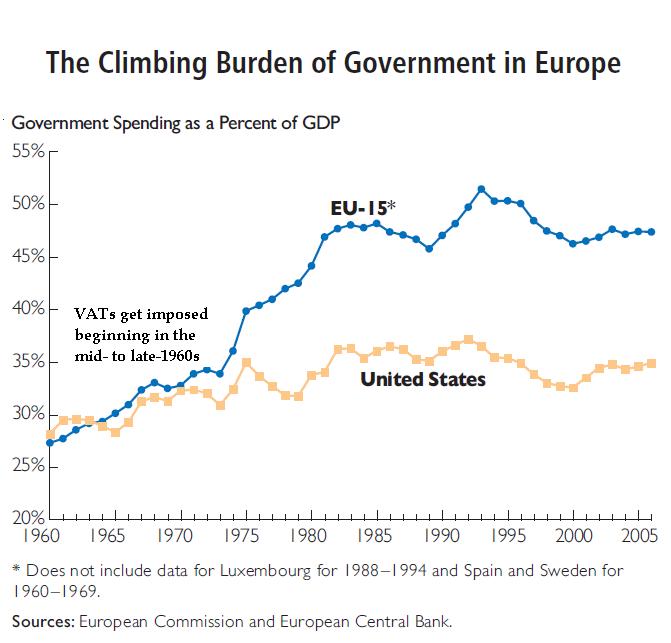

Simply stated, this hidden type of national sales tax was a key precursor for the expansion of the European welfare state. As you can see in the chart, the burden of government spending in Europe after World War II was similar to the size of the public sector in the United States.

Then European governments began to adopt the VAT in the late 1960s. Those VATs quickly expanded and became money machines for more spending (and more debt!).

Needless to say, the United States should not make the same mistake. Bigger government has led to worse economic outcomes in Europe, as I’ve documented in my four-part series (here, here, here, and here).

Financing bigger government with a VAT would weaken economic performance. In a 2010 study for the Mercatus Center, Professor Randall Holcombe crunched some numbers and reached some depressing conclusions.

…the effect of various VAT rates on GDP looking 10 years out and 20 years out. …In the revenue-enhancement case, where VAT revenue adds to existing sources of tax revenue, a 3 percent VAT would exact a 2.1 percent GDP penalty by 2020 and a 3.7 percent GDP penalty by 2030. A 5 percent VAT rate would bring with it a 3 percent GDP penalty by 2020 and a 5.6 percent GDP penalty by 2030. A 7 percent VAT rate…would reduce GDP by 4.1 percent by 2020 and 7.5 percent by 2030.

And here’s one of his tables, showing the negative effect on economic output (as well as some calculations showing that the VAT would not collect as much money as supporters hope).

Now let’s look at some more-recent research.

In 2024, Adam Michel wrote a report on the tax implications of bigger government.

Here’s his section on the VAT.

…consumption taxes (taxes on goods and services) account for almost three times as much revenue in the EU countries than in the United States. Every European country uses a value-added tax (VAT), a type of national sales tax collected by businesses at each stage of production instead of at the point of sale. In the United States, most consumption tax revenue is collected by state governments through a point-of-sale retail sales tax. In 2022, the average standard VAT rate in the EU countries was 21.8 percent, and the average state and local sales tax rate in the US was 6.6 percent. EU country VATs raise revenue equal to 12 percent of GDP, compared to sales taxes, which collect 4.3 percent of GDP in the United States. The adoption of VATs is closely associated with government growth because new revenue sources, especially when the cost of the tax is not transparent, tend to fuel new public expenditures and reduce pressure on spending reforms. This association is evident in the reliance on VAT revenue across EU countries, where governments are almost 20 percent larger than in the United States.

Here’s Adam’s chart, showing how the absence of a VAT is the main reason the United States has a fiscal advantage over the European Union.

While in Sweden last week, I wrote several columns (here, here, and here) about that nation’s fiscal policy.

But I also had a discussion about American fiscal policy with one of the tax experts at the Confederation of Swedish Enterprise. That included a discussion of the value-added tax (VAT).

If you don’t want to spend a few minutes watching the video, I made two theoretical observations and two practical observations.

A VAT has the same “tax base” as a flat tax. The structural difference is that a flat tax takes a slice of your income as you earn and a VAT takes a slice of your income as you spend.

But we’ll never be given a chance to make that swap.

Instead, some people claim that we are facing a different type of choice. Should we finance our (baked-in-the-cake) expanding burden of government with class-warfare taxes or a value-added tax?

The right answer, needless to say, is to restrain spending. But if someone is holding a gun to your head and demanding that you choose a tax increase, which one do you pick?

Seems like a VAT would be the less-harmful approach, but this is a good opportunity to raise my two practical points.

In the real world, adoption of a VAT almost surely will lead to more class warfare taxes because politicians will want to balance the harm to lower-income people by also imposing taxes that hurt higher-income people.

To help reinforce that argument, here’s a new map from the Tax Foundation showing VAT rates on the other side of the Atlantic Ocean.

With a few exceptions (notably Switzerland), these hidden taxes are enormous burden. Indeed, the average EU VAT rate is approaching 22 percent, a huge increase over the past five decades.

From a tax policy perspective, high VAT rates are misguided since they increase the gap between pre-tax income and post-tax consumption. And lower-income households are especially disadvantaged.

But high VAT rates also are misguided since they enable bigger burdens of government spending.

Here’s a chart based on OECD tax data and OECD spending data. As you can see, when compared to the United States, higher VAT burdens among EU/OECD members are associated with higher spending burdens.

I wrote yesterday to criticize Andrew Biggs of the American Enterprise Institute and Alicia Munnell of Boston College for suggesting a $3 trillion 10-year tax increase on IRAs and 401(k)s.

And this point is especially relevant because today’s column is going to analyze another giant tax increase being advocated by someone at the American Enterprise Institute.

A value-added tax (VAT) is an essential component… The United States should follow the lead of 170 other countries and territories by adding a VAT… We should act sooner rather than later to limit the debt buildup and ease the fiscal burden on future generations. …there is no viable way to fully address the fiscal imbalance without middle-class tax increases. …The European Union, the International Monetary Fund, and the World Bank have promoted the VAT. …To be sure, the VAT is not as economically efficient as entitlement benefit cuts. Notably, a VAT (or a retail sales tax) creates work disincentives similar to those created by income taxes. …When addressing the fiscal imbalance, time is not on our side. To promote long-term economic growth and ease the fiscal burden on future generations, we should adopt a VAT sooner rather than later.

I’m not sure why Viard thinks copying bad policies of other countries is a good idea. Especially since the United States is much richer than about 98 percent of those nations. Seems like they should be copying us.

But the main point I want to get across is that it is utterly naive to think that giving politicians a huge source of additional revenue will lead to less debt.

Why do I say that?

For the simple reason that the nations most similar to the United States tried Viard’s approach and the results were horrible.

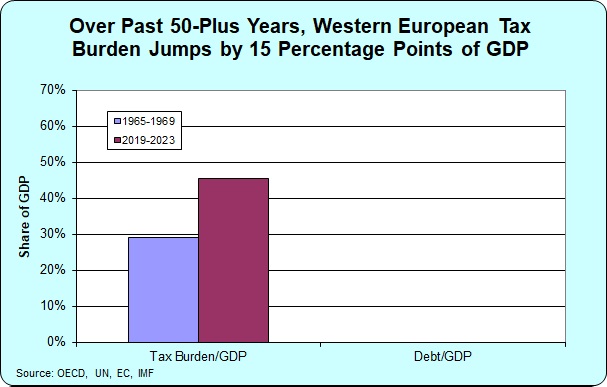

I’m going to recycle three charts from last year. The first one shows that the tax burden increased dramatically in Western Europe over the past 50-plus years – in large part because all those nations adopted big value-added taxes.

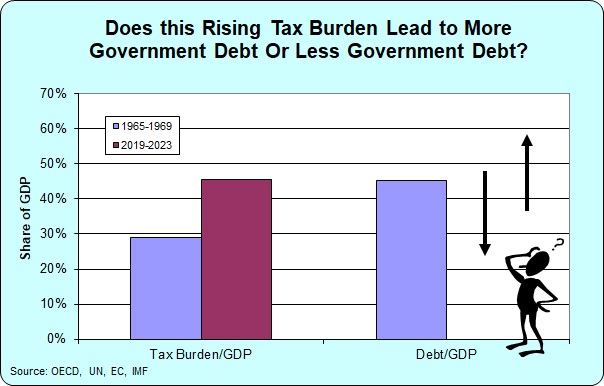

My second chart than asked whether those massive tax increases in Europe reduced the debt, which averaged about 45 percent of GDP in the late 1960s.

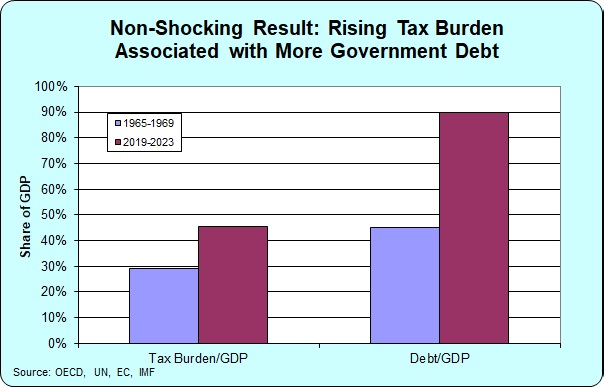

The answer, unsurprisingly, is that debt increased. Dramatically.

Politicians spent every single penny of the additional revenue. And then spent even more.

So much more spending that debt in Western Europe now averages 90 percent of GDP, two times higher than it was before value-added taxes were imposed.

Needless to say, Viard did not address that point in his testimony.

But someone did touch on that issue when testifying to many years ago.

Here’s what that charming and lovable person said.

P.S. In the above charts, I used averages for five-year periods so that nobody could accuse me of cherry-picking a single year that might not be representative of actual trends.

P.P.S. Some readers may be wondering if debt skyrocketed in Europe because of emergency pandemic spending instead of the value-added tax. Nope. I also did similar sets of charts in 2012 and 2016 and you see the same pattern. All that has changed is that taxes, spending, and debt get higher every time I update the numbers.

But only in theory. In reality, we have gobs of evidence (even from the New York Times, albeit inadvertently) that budget deals with higher taxes don’t work.

The reason is that politicians can’t resist the temptation to increase spending whenever they think more tax revenue might be available.

In other words, Milton Friedman was right when he warned that “History shows that over a long period of time government will spend whatever the tax system raises plus as much more as it can get away with.”

Unfortunately, some people don’t understand history. Or they don’t care.

For instance, Fareed Zakaria argues in the Washington Post that politicians should impose a value-added tax. Here are some excerpts.

Total debt is now more than $33 trillion, the deficit is over 7 percent of gross domestic product, and this year’s net interest payment on the debt will probably be over $650 billion… For almost a generation, policymakers have been able to avoid seriously confronting deficits… Fortunately, there is a simple solution staring us in the face… Adopt a national sales tax, like every other advanced economy in the world. …According to the Congressional Budget Office, a broad 5 percent tax of this kind could raise $3 trillion over the next decade… On average, European Union countries get roughly 20 percent of their tax revenue from a VAT; the United States is getting zero. …It is time for the United States to join more than 160 other countries with a value-added tax and ask all Americans to chip in to set the country on a firmer fiscal path for decades.

Zakaria’s numbers are accurate. A VAT would raise a lot of money, as predicted by the CBO. And European nations generate a lot of VAT revenue.

But what about his analysis? Is Zakaria correct that a VAT would put America on “a firmer fiscal path”?

Since he cites Europe, let’s look at the evidence. I did this back in 2012, looking at the nations in Western Europe that are most similar to the United States, and comparing tax and debt levels both before and after value-added taxes.

And I did the same thing in 2016. In both cases, I used five-year averages to ensure that the numbers were not misleading because of the business cycle or anything else that might produce quirky data for a year or two.

In both cases, I found that politicians imposed massive tax increases, with VATs playing a big role. But I also discovered that politicians spent even more money (just as Friedman predicted), so the net result was more red ink.

Let’s now update that research.

We’ll start with this chart, which shows yet again that there has been a massive increase in tax revenue in Western European nations over the past five-plus decades.

If Zakaria and other pro-tax increase people are right, all that new revenue should have produced “a firmer fiscal path” of less debt.

Our second chart shows that government debt in the late 1960s averaged about 45 percent of GDP in Western Europe.

So what actually happened?

Did debt get paid off? Did debt get reduced? Was Western Europe put on “a firmer fiscal path”?

Of course not

As shown in our final chart, debt levels in the past five-plus decades have doubled to nearly 90 percent of GDP.

By the way, I’m mixing and matching data from several sources, so I’m sure that the numbers from the late 1960s are not a perfect match for the IMF numbers I used for 1919-2023.

That being said, there’s no arguing with the core finding. Massive revenue increases resulted in much higher levels of red ink because politicians increased the burden of government spending even faster.

That argument is compelling when I’m speaking to conservatives (though not all of them, apparently!), but I need different arguments when talking to my friends on the left.

Fortunately, I now have some very persuasive data that hopefully will make left-of-center types much less likely to support a VAT.

Look at this graph, which clearly shows a strong relationship between higher value-added taxes and higher poverty.

The chart comes from a recent study by Manuel Schechtl for Social Policy and Society, published by Cambridge University Press.

He investigated the extent to which valued-added taxes push households into poverty.

Poor households spend a higher share of their disposable income on consumption simply because consumption does not increase proportionally with income. …This study aims to evaluate the change in poverty rates before and after deducting consumption taxes (consumable income poverty) and the increase in poverty (consumption tax induced poverty) across household types. …Figure 2 indicates the overall percentage point increase in poverty plotted against the implicit consumption tax rate. The pattern reveals a clear positive association between consumption tax and poverty increase – for instance, consumption taxes in Slovenia and Hungary lead to an increase in poverty of over ten percentage points compared to about four percentage points in Mexico or Switzerland (which have lower implicit consumption tax rates).

Very depressing findings, at least for those of us who don’t like high taxes.

But there is a big methodological flaw in the study.

It relies on a dishonest definition of poverty, one that is used by ideologues who want to exaggerate societal problems.

…poverty is measured as below fifty percent of median disposable household income.

For what it is worth, this approach measures the distribution of income in a society, not material deprivation or some other tangible definition of actual poverty.

Having pointed out this flaw, I don’t know if the author is trying to be dishonest. He may have simply relied on data from a group (like the OECD) that does have a dishonest agenda.

However, this methodological flaw does not undermine Schechtl’s core point. There’s no question that value-added taxes reduce the ability of poor people to consume. And I would not be surprised if a chart based on honest data looked very similar to the one shown above.

The moral of the story is that all good people – on the right and on the left – should reject the value-added tax.

P.S. One of the reasons I get upset about the Biden/Trump approach to entitlements is that I fear it would make a VAT more likely.

I frequently share this chart, for instance, that shows that the nations in Western Europe were quite similar to the United States back in the 1960s, with government budgets that consumed about 30 percent of economic output.

That was before they enacted VATs.

But once European politicians got that new source of revenue, the spending burden diverged, with the welfare state becoming a much larger burden in Western Europe than in the United States.

That argument is just as accurate today as it was back in 2011.

For today’s column, however, I want to focus on what I said in the last minute of my testimony (beginning about 4:00).

I pointed out that VAT supporters are wrong when they claim that adoption of this new tax would enable reductions in the income tax.

And if you peruse my written testimony, you’ll see that I included several charts showing how tax burdens changed between 1965 and 2008. In every case, I showed that European politicians actually increased the burden of income taxes after they enacted their VATs.

Is that still true?

Of course.

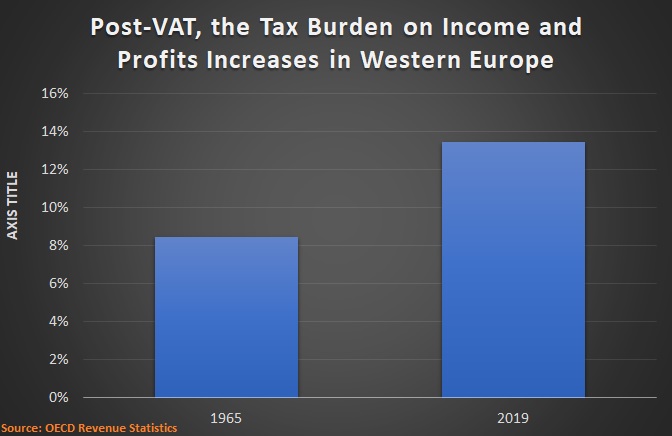

Here’s an updated version of the chart showing that the overall tax burden dramatically increased after VATs were imposed.

In the United States, by contrast, the overall tax burden only increased during this time period from 23.6 percent of GDP to 25 percent of GDP.

Still bad news, but nowhere near as bad as Western Europe, where the overall tax burden jumped by more than 13 percentage points.

Now let’s peruse the updated version of the chart showing what happened to taxes on income and profits.

As you can see, European governments definitely did not use VAT revenues to lower other taxes.

In the United States, by contrast, the tax burden on income and profits only increased during this time period from 11.3 percent of GDP to 11.6 percent of GDP.

Still bad news, but nowhere near as bad as Western Europe, where the tax burden on income and profits jumped by nearly 5 percentage points.

Now let’s peruse the updated version of the chart showing what happened to taxes on corporations (this chart is especially important because there are very naive people in the business community who think that they can avoid higher taxes on their companies if they surrender to a VAT).

As you can see, governments in Europe have been grabbing more money from corporations since VATs were imposed.

In the United States, by contrast, the tax burden on corporations actually decreased during this time period from 3.9 percent of GDP to 1.3 percent of GDP.

But that’s about as likely as me playing the outfield for the New York Yankees in this year’s World Series.

P.S. I mentioned at the very end of my testimony that we did not have clear evidence from other nations that subsequently adopted VATs. In the case of Japan, we now do have data showing how the VAT is financing bigger government.

P.P.S. Some VAT advocates actually claim the levy is good for growth. That’s a nonsensical claim. VATs drive a wedge between pre-tax income and post-tax consumption. What they really mean to say is that VATs don’t do as much damage, on a per-dollar-raised basis, as conventional income taxes (with punitive rates and double taxation).

P.P.P.S. You can enjoy some good anti-VAT cartoons here, here, and here.

Consider, for instance, Alan Viard of the American Enterprise.

He wrote a column last November arguing that we should let politicians in Washington have this new source of tax revenue, and I explained why his arguments were wrong.

But I’m obviously not very persuasive since he just reiterated his support for a VAT in an interview with the Dallas Federal Reserve Bank. Here are some of the highlights (lowlights might be a better term).

…tax increases on corporations and high-income households as well as benefit cuts could be part of a debt-reduction package…such tax increases would have limited revenue potential. …a VAT should—and undoubtedly would—be accompanied by rebates to offset the tax burden on low-income households. The Tax Policy Center estimated that a 7.7 percent VAT with rebates, which would raise the same net revenue as a 5 percent VAT without rebates, would generally be progressive. …the VAT would be only one component of the federal tax system. Individual and corporate income taxes would continue to add progressivity.

There are two remarkable admissions in the above excerpts.

He’s basically admitting a VAT would be accompanied by class-warfare tax hikes on companies and households – thus undermining the usual argument that the VAT is needed to avert these other types of tax increases.

He’s basically admitting a VAT would be accompanied by a new entitlement program of “rebates” – thus undermining the argument that VAT revenues would be used to reduce deficits and debt.

But what I found particularly amazing is that Viard never tries to empirically justify his main argument that, a) debt is a problem, and b) the VAT is part of a solution.

I don’t particularly object to the first part (though I would argue the real problem is spending). But the assertion that a VAT will solve that problem is contrary to real-world evidence.

For instance, government debt has continued to grow ever since Japan adopted a VAT.

Public finance experts sometime differ in how to describe a value-added tax.

Is it a hidden form of a national sales tax, imposed at each stage of the production process?

Is it a hidden withholding tax on income, imposed at each stage of the production process?

Both answers are actually correct. The VAT is both a tax on consumption and a tax on income because – notwithstanding its other flaws – it has the right “tax base.”

In other words, like the flat tax, a VAT taxes all economic activity, but only one time (i.e., no double taxation of income that is saved and invested). And it usually has a single rate, which is another feature of a flat tax.

That’s why a VAT (in theory!) would be acceptable if it was used to finance the complete abolition of the income tax.

But that’s not a realistic option. Heck, it’s not even an unrealistic option.

Instead, many politicians in the United States want to keep the income tax and also impose a VAT so they can finance a bigger burden of government – which is exactly what’s been happening in Europe.

Unfortunately, they’re getting some support from the American Enterprise Institute. Alan Viard, a resident scholar at AEI, has a new column urging the adoption of a VAT.

Let’s review what he wrote and explain why he’s wrong.

The U.S. faces a large long-term imbalance between projected federal tax revenue and federal spending… To narrow the fiscal imbalance, we should follow the lead of 160 other countries by adopting a value-added tax (VAT), a consumption tax that is economically similar to a retail sales tax. …Adopting a VAT would significantly curb the debt buildup.

I’ve never been impressed with the argument that the U.S. should adopt a policy simply because other nations have done the same thing.

The United States is much richer than other countries in large part because we haven’t replicated their mistakes. So why start now?

But let’s deal with Viard’s assertion that a VAT would “significantly curb the debt buildup.”

I recently showed the opposite happened in Japan. They adopted a VAT (and have repeatedly increased the VAT rate), but debt has increased.

But I think the strongest evidence is from Europe since we have several additional decades of data. Those nations started imposing VATs in the late 1960s and they now all have very high VAT rates.

The moral of the story is that Milton Friedman was right when he warned that, “History shows that over a long period of time government will spend whatever the tax system raises plus as much more as it can get away with.”

So why would Viard support a VAT when the evidence overwhelmingly shows that a big tax increase will worse a nation’s fiscal outlook?

He argues that a VAT would be the least-worst way to finance bigger government.

Although tax increases on the affluent place the burden on those with the most ability to pay, they impede long-run economic growth by penalizing saving and investment and distorting business decisions. The economic costs become larger as tax rates are pushed higher. …The VAT is more growth-friendly than high-income tax increases because it does not penalize saving and investment and poses fewer economic distortions.

He’s right that a VAT doesn’t do as much damage as class-warfare tax, but he’s wildly wrong to assert that it is “growth-friendly.”

Simply stated, a VAT will drive a further wedge between pre-tax income and post-tax consumption. That not only will discourage work. It also will discourage saving and investment.

The only positive thing to say is that a VAT doesn’t discourage those good things as much as some other types of tax increases.

But that’s sort of like saying that it’s better to lose your hand in an accident instead of losing your entire arm. Call me crazy, but I think the best outcome is to avoid the accident in the first place.

I’ll close by debunking the notion that a VAT is a simple tax.

As you can see from this European map, VATs can impose huge complexity burdens on businesses.

Yes, the map shows that some nations have relatively simple VATs, but American politicians already have shown with the income tax that they can’t resist turning a tax system into a Byzantine nightmare. Of course they would do the same with the VAT, creating special loopholes and penalties to please their donors.

P.S. Here’s my video from 2009, which explains how a VAT works and why it would be a bad idea.

Back in 2012, I warned that the value-added tax (a hidden version of a national sales tax) was enabling bad fiscal policy in Japan, in large part because politicians wouldn’t make much-needed entitlement reforms if they had the option of raising the VAT.

Later that year, I repeated my warning, noting that politicians in Japan were becoming increasingly vocal about grabbing more money.

Unsurprisingly, these warnings had no effect. In 2013, Japan’s politicians announced the VAT would increase the following year.

Needless to say, Japan’s politicians didn’t learn from this mistake. Notwithstanding my warnings in 2018 and 2019, they just increased the VAT yet again.

So how’s that working out for them?

In a column for the Wall Street Journal, Mike Bird discusses the economic impact of the most-recent increase in the value-added tax.

Japan’s economy shrank sharply in the final three months of 2019, logging its second-worst quarter in the past decade. That would be easier to stomach if it weren’t because of a mistake policy makers have now made three times. In October, Japan raised its sales tax to 10% from 8%—and spending tanked. Household consumption fell 11.5% on an annualized basis in the October-December quarter, fueling a 6.3% fall in annualized gross domestic product. Sales-tax increases in 1997 and 2014 likewise knocked the economy off course. The three worst quarters for household consumption in the past quarter-century were those in which sales tax was raised. …the thinking that led to such destructive behavior is bizarrely resilient.

Here’s the accompanying chart, which shows how every increase in the VAT caused a drop in consumption.

For what it’s worth, I don’t find this chart very persuasive.

Yes, consumption drops in the short run when there’s an increase in the VAT, but there doesn’t seem to be any impact on the long-run trend.

But I’m digressing. Let’s get back to Japan’s VAT mistake.

The Wall Street Journalopined on the issue earlier this week.

The third time wasn’t the charm for Tokyo’s long-running attempt to increase its consumption tax. Data released Monday show Japan’s economy contracted in the last three months of 2019 as the tax hike hammered growth—as many warned and like the previous two times the tax has been raised since its 1989 introduction, in 1997 and 2014. …Wage growth is anemic despite a tight labor market, and the Labor Ministry calculates that inflation-adjusted pay fell 3.5% from 2012-2018. The tax rise creates a new and higher squeeze on household incomes. …The usual suspects are now calling for more Keynesian spending on public works and social spending. Three decades of similar blowouts have created the fiscal mess that always becomes justification for more consumption-tax hikes. …It’s too late for Japan to avoid the costs of Mr. Abe’s economic failures. But other governments can learn the lessons that Japan’s leaders refuse to heed.

Unfortunately, other leaders aren’t learning the right lessons.

Let’s close by citing three additional sentences from the WSJ editorial.

The fiscal pyromaniacs at the IMF want even further VAT increases in Japan.

The International Monetary Fund thinks the consumption-tax rate will have to rise to 15% over the next decade, and to 20% by 2050. But first the fund’s wizards say Tokyo must expand its Keynesian spending to make the economy “strong” enough to bear the tax hikes to pay for the spending. Got that?

I wrote last year about the IMF’s perverse fixation on ever-increasing VAT burdens in Japan, so I’m not surprised that the international bureaucracy is continuing its campaign.

It enables politicians to siphon money from the productive sector of the economy, whether we’re looking at poor nations or rich nations.

By contrast, it’s difficult to generate more revenue from the personal income tax because of the Laffer Curve.

P.S. Some VAT advocates actually claim the levy is good for growth. That’s a nonsensical claim. VATs drive a wedge between pre-tax income and post-tax consumption. What they really mean to say is that VATs don’t do as much damage, on a per-dollar-raised basis, as conventional income taxes (with punitive rates and double taxation).

I wrote yesterday about Japan’s experience with the value-added tax, mostly to criticize the International Monetary Fund.

The statist bureaucrats at the IMF are urging a big increase in Japan’s VAT even though the last increase was only imposed two months ago (in a perverse way, I admire their ability to stay on message).

Today, I want to focus on a broader lesson regarding the political economy of the value-added tax. Because what’s happened in Japan is further confirmation that a VAT would be a terrible idea for the United States.

Simply stated, the levy would be a recipe for bigger government and more red ink.

Let’s look at three charts. First, here’s a look at how politicians in Japan have been pushing the VAT burden ever higher.

What’s been the result? Have politicians used the money to lower other taxes? Have they used the money to reduce government debt?

Hardly. As was the case in Europe, the value-added tax in Japan is associated with an increase in the burden of spending.

Here’s a chart (based on the IMF’s own data) showing that government is now consuming almost 35 percent of economic output, up from about 30 percent of GDP when the VAT was first imposed.

I’ve added a trend line (automatically generated by Excel) to illustrate what’s been happening. It’s not a big effect, but keep in mind the VAT never climbed above 5 percent until 2014.

Now let’s look at some numbers that are very unambiguous.

Japan’s politicians imposed the VAT in part because they claimed it was a way of averting more red ink.

Yet our final chart shows what’s happened to both gross debt and net debt since the VAT was imposed.

To be sure, the VAT was only one piece of a large economic puzzle. If you want to finger the main culprits for all this red ink, look first at Keynesian spending binges and economic stagnation.

But we also know the politicians were wrong when they said a VAT would keep debt under control

But it’s very unlikely that a VAT will be imposed on the United States by the left. At least not acting alone.

The real danger is that we’ll wind up with a VAT because some folks on the right offer their support. These people don’t particularly want European-type levels of redistribution, but they think that’s going to happen. So one of their motives is to figure out ways to finance a large welfare state without completely tanking the economy.

They are right that a VAT doesn’t impose the same amount of damage, on a per-dollar-collected basis, as higher income tax rates. Or increases in double taxation (though it’s important to realize that it would still penalize productive behavior by increasing the wedge between pre-tax income and post-tax consumption).

But their willingness to surrender is nonetheless very distressing.

The bottom line is that the most important fiscal issue facing America is the need for genuine entitlement reform. Achieving that goal is an uphill battle. But if politicians get a big new source of revenue, that uphill battle becomes an impossible battle.

But now the IMF is upping the ante by adding its bad advice on tax policy.

Japan’s politicians raised the value-added tax just two months ago.

But that’s not enough for the IMF. The bureaucrats already are urging a far bigger increase in the levy.

Japan needs to raise its consumption tax further to fund growing social security costs, the International Monetary Fund recommended… The tax “would need to increase gradually” to 15% by 2030 and 20% by 2050, the IMF said in a report. …IMF Managing Director Kristalina Georgieva praised the smooth implementation of the Oct. 1 hike that took the consumption tax to 10% from 8%.

Needless to say, one of the main lessons from this sordid experience is that it’s never a good idea to give politicians a new source of revenue.

Look at what’s happened ever since the VAT was first imposed in 1989.

And now the IMF wants to push the rate up to 15 percent. And then 20 percent.

By the way, it’s worth noting that Japan’s politicians actually welcome this bad advice.

The nation faces a big demographic crunch (increasing life expectancy and low birth rates), and that means entitlement spending is on track to consume an ever-larger share of economic output.

To give you an idea of what’s happening, here’s a chart from the IMF’s report on Japan. It only looks at health-related spending, so keep in mind that the red line would be significantly hihger if Japan’s version of Social Security was included.

The bottom line is that Japan’s politicians want options to finance a growing burden of government spending.

Sadly, the IMF is more than happy to rationalize that bad approach.

P.S. Japan’s politicians could reform entitlements, of course, but don’t hold your breath waiting for that to happen. Instead, expect this “depressing chart” to get even more depressing.

And the ever-sensible Swiss, in a 2016 referendum, overwhelmingly rejected universal handouts.

Needless to say, it also would be a catastrophic mistake to give Washington several new sources of revenue to finance this scheme. A big value-added tax would be especially misguided.

Let’s take a closer look at Yang’s plan. As I noted in the interview, the Tax Foundation crunched the numbers.

Andrew Yang said he wants to provide each American adult $1,000 per month in a universal basic income (UBI) he calls a “Freedom Dividend.” He argued that this proposal could be paid for with…a combination of new revenue from a VAT, other taxes, spending cuts, and economic growth. …We estimate that his plan, as described, could only fund a little less than half the Freedom Dividend at $1,000 a month. A more realistic plan would require reducing the Freedom Dividend to $750 per month and raising the VAT to 22 percent.

If you’re interested, here are more details about his plan.

…individuals would need to choose between their current government benefits and the Freedom Dividend. As such, some individuals may decline the Freedom Dividend if they determine that their current government benefits are more valuable. The benefits that individuals would need to give up are Supplemental Nutritional Assistance Program (SNAP), Temporary Assistance for Needed Families (TANF), Supplemental Security Income (SSI), and SNAP for Women, Infants, and Child Program (WIC). To cover the additional cost of the Freedom Dividend, Yang would raise revenue in five ways: A 10 percent VAT…A tax on financial transactions…Taxing capital gains and carried interest at ordinary income rates…Remove the wage cap on the Social Security payroll tax…A $40 per metric ton carbon tax.

By the way, Yang has already waffled on some of his spending offsets, recently stating that the so-called Freedom Dividend wouldn’t replace existing programs.

In any event, the economic and budgetary effects would be bad news.

…his overall plan would reduce the long-run size of the economy and the tax base. The three major taxes in his plan (VAT, carbon tax, and payroll tax increase), while efficient sources of revenue, would tend to reduce labor force participation by reducing the after-tax returns to working. Using the Tax Foundation Model, we estimate that the weighted average marginal tax rate on labor income would increase by about 8.6 percentage points. The resulting reduction in hours worked would ultimately reduce output by 3 percent. We estimate that Yang would lose about $124 billion each year in revenue due to the lower output.

P.S. When the Tax Foundation say a tax is an “efficient source of revenue,” that means that it would result in a modest level of economic damage on a per-dollar-collected basis. This is why they show a rather modest amount of negative revenue feedback (-$124 billion).

I think they’re being too kind. Extending the Social Security payroll tax to all income would result in a huge increase in marginal tax rates on investors, entrepreneurs, and other high-income taxpayers. As explained a few days ago, those are the people who are very responsive to changes in tax rates.

There’s general agreement among public finance experts that personal income taxes and corporate income taxes, on a per-dollar-collected basis, do the most economic damage.

And I suspect there’s a lot of agreement that this is because these levies often have high marginal tax rates and often are accompanied by a significant bias against income that is saved and invested.

Payroll tax and consumption taxes, by contrast, are thought to be less damaging because they generally don’t have “progressive rates” and they are “neutral,” meaning they rarely involve any double taxation of saving and investment.

But “less damaging” is not the same as “no damage.”

Such taxes still drive a wedge between pre-tax income and post-tax consumption, so they do result in less economic activity (what economists refer to as “deadweight loss“).

And the deadweight loss can be significant if the overall tax burden is sufficiently onerous (as is the case in many European nations).

Interestingly, the (normally pro-tax) International Monetary Fund just released a study on this topic. It looked at the impact of taxes on work in the new member states (NMS) of the European Union. Here’s a summary of what the authors wanted to investigate.

Given demographic and pension pressures facing many EU28 countries amidst low labor market participation rates together with still high tax wedges, the call to review public policies has gained renewed prominence in the EU political debate. …tax wedges remain high and participation rates, while having increased importantly in a few countries over 2000-17 , are still around or below 70 percent in many of them. This hints at the need for addressing structural problems to improve economic fortunes. In this paper we focus our attention on hours worked (per working age population). …At country level, hours worked reflect labor supply decisions and could be thought of a measure of labor utilization. Long-run changes in labor supply are driven by incentives, of which taxes are perceived to be central. Assessing the importance of taxation on hours is key to provide new insights for potential policy actions.

And here’s what they found.

We study the role of taxes in accounting for differences in hours worked across NMS over the 1995-17 period… We find that consumption and labor taxes significantly discourage labor supply and can explain close to 21 percent of the observed variation of hours across NMS. …Higher tax rates reduce households’ net labor income and real purchasing power, inducing them to substitute consumption for leisure, which cannot be taxed. …Our findings show that, conditional on other factors, taxes are an important determinant of hours. Point estimates suggest a high elasticity of hours to taxes (close to 0.5), which is robust to the inclusion of other factors.

What’s interesting about the new member states of Eastern Europe is that many of them have flat taxes and low corporate rates.

So the personal and corporate income taxes are not a major burden.

But they so have relatively high payroll taxes (a.k.a., social insurance taxes) and relatively onerous value-added taxes.

So it’s hardly a surprise that these levies are the ones most associated with deadweight loss.

We find that social security contributions deter hours the most, followed by consumption taxes and, to a lesser extent, personal income taxes. …Consumption and personal income taxes are found to affect hours per worker, but not employment rates. On the other hand, social security contributions are negatively associated with employment rates, but do not seem to affect hours per worker. …In line with the literature, we document that women’s employment rate is more sensitive to changes in tax policies. We find the elasticity of employment rate to social security contributions to be 7 percent larger for women vis-à-vis men.

Here’s one of the charts from the study.

And here’s an explanation of what it means.

Figure 4 shows the evolution of hours and effective taxes. Hours worked increased substantially for Group 1, while it remained stable in Group 2 (Panel (a)). In both groups, the effect of the GFC is noticeable as hours sharply declined after 2008. Panel (b) shows the evolution of the average effective tax rate in each group. Interestingly, countries in Group 1, which observed an increase in hours, had lower effective tax rates (below 40 percent) throughout the period. In addition, we observe a negative correlation between hours and taxes for most of the sample. For Group 1, the large increase in hours – between year 2000 and the GFC – happened at the same time taxes declined

Here’s another chart from the IMF report.

And here’s some of the explanatory text.

Figure 5 depicts the relationship between hours worked and taxes across countries. In Panel (a), we observe a negative correlation between hours and taxes in levels for each group, with the negative correlation being stronger in Group 2 than in Group 1 (it has a steeper slope). Panel (b) shows total log changes in hours and taxes throughout the period. It also displays a negative correlation.

Looking at the conclusion, a key takeaway from the study is that there is a substantial loss of economic activity because of theoretically benign (but in reality onerous) taxes on consumption and labor.

Our modelling exercise shows that taxes influence the long-run trend in hours and our econometric exercise shows that the findings are robust to the inclusion of other labor market determinants. Furthermore, we document an elasticity of hours to overall taxes close to 0.5. We find that differences in tax burden can explain up to 21 percent in the variation of hours worked across NMS. The main takeaway of this study is that excessive tax burden, either in the form of consumption or labor taxes, can lead to substantial deadweight losses in terms of labor supply. .. overall tax burden – and not only labor taxes – should be considered when thinking about incentives from tax schemes.

Yes, incentives do matter.

And it’s good that an IMF report is providing good evidence for lower tax rates.

A couple of weeks ago, I used a story about a local tax issue in Washington, DC, to make an important point about how new tax increases cause more damage than previous tax increases because “deadweight losses” increase geometrically rather than arithmetically.

Simply stated, if a tax of X does Y amount of damage, then a tax of 2X will do a lot more damage than 2Y.

As such, I was very interested to see a new study on this topic from the World Bank. It starts by noting that higher tax rates are the wrong way to address fiscal shortfalls.

…studies have used the narrative approach for individual or multi-country analyses (in all cases, focusing solely on industrial economies, and mostly on industrial European countries). These studies find large negative tax multipliers, ranging between 2 and 5. This recent consensus pointing to large negative tax multipliers, especially in industrial European countries, naturally entails important policy prescriptions. For example, as part of a more comprehensive series of papers focusing on spending and tax multipliers, Alesina, Favero, and Giavazzi (2015) point that policies based upon spending cuts are much less costly in terms of short run output losses than tax based adjustments.

The four authors used data on value-added taxes to investigate whether higher tax rates did more damage or less damage in developing nations.

A natural question is whether large negative tax multipliers are a robust empirical regularity… In order to answer this highly relevant academic and policy question, one would ideally need to conduct a study using a more global sample including industrial and, particularly, developing countries. …This paper takes on this challenge by focusing on 51 countries (21 industrial and 30 developing) for the period 1970-2014. …we focus our efforts on building a new series for quarterly standard value-added tax rates (henceforth VAT rates). …We identify a total of 96 VAT rate changes in 35 countries (18 industrial and 17 developing).

The economists found that VAT increases did the most damage in developing nations.

…when splitting the sample into industrial European economies and the rest of countries, we find tax multipliers of 3:6 and 1:2, respectively. While the tax multiplier in industrial European economies is quite negative and statistically significant (in line with recent studies), it is about 3 times smaller (in absolute value) and borderline statistically significant for the rest of countries.

Here’s a chart showing the comparison.

Now here’s the part that merits close attention.

The study confirms that the deadweight loss of VAT hikes is higher in developed nations because the initial tax burden is higher.

Based on different types of macroeconomic models (which in turn rely on different mechanisms), the output effect of tax changes is expected to be small at low initial levels of taxation but exponentially larger when initial tax levels are high. Therefore, the distortions and disincentives imposed by taxation on economic activity are directly, and non-linearly, related to the level of tax rates. By the same token, for a given level of initial tax rates, larger tax rate changes have larger tax multipliers. …In line with theoretical distortionary and disincentive-based arguments, we find, using our novel worldwide narrative, that the effect of tax changes on output is indeed highly non-linear. Our empirical findings show that the tax multiplier is essentially zero under relatively low/moderate initial tax rate levels and more negative as the initial tax rate and the size of the change in the tax rate increase. …This evidence strongly supports distortionary and disincentive-based arguments regarding a nonlinear effect of tax rate changes on economic activity…the economy will inevitably suffer when taxes are increased at higher initial tax rate levels.

So if taking a high VAT rate and making it even higher causes a disproportionate amount of economic damage, then imagine how destructive it is to increase top income tax rates.

P.S. The fact that a VAT is less destructive than an income tax is definitely not an argument for enacting a VAT. That would be akin to arguing that it would be fun to break your wrist because that wouldn’t hurt as much as the broken leg you already have.

I’ve even dealt with people who actually argue that a VAT isn’t economically destructive because it imposes the same tax on current consumption and future consumption. I agree with them that it is a good idea to avoid double taxation of saving and investment, but that doesn’t change the fact that a VAT increases the wedge between pre-tax income and post-tax consumption.

Panels A and B in Figure 18 show the relationship between the VAT rate a and the perceived effect of taxes on incentives to work and invest, respectively, for a sample of 123 countries for the year 2014. Supporting our previous findings, the relationship is highly non-linear. While the perceived effect of taxes on the incentives to work and invest barely changes as VAT rates increase at low/moderate levels (approximately until the VAT rate reaches 14 percent), it falls rapidly for high levels of VAT rates.

P.S. Not everyone understands this common-sense observation. For instance, the bureaucrats at the Congressional Budget Office basically argued back in 2010 that a 100 percent tax rate was the way to maximize growth.

The value-added tax was first imposed in Europe starting about 50 years ago. Politicians in nations like France approve of this tax because it is generally hidden, so it is relatively easy to periodically raise the rate.

And that’s the reason I am vociferously opposed to the VAT. I don’t think it’s a coincidence that the burden of government spending dramatically increased in Europe once politicians got their hands on a new source of revenue.

We’ll start by crossing the Pacific to see what’s happening in Japan, as reported by Reuters.

Japanese Prime Minister Shinzo Abe vowed to proceed with next year’s scheduled sales tax hike “by all means”… Abe said his ruling Liberal Democratic Party (LDP) won last year’s lower house election with a pledge to use proceeds from the sales tax increase to make Japan’s social welfare system more sustainable. …his plan to raise the tax to 10 percent from 8 percent in October next year. Abe twice postponed the tax hike after an increase to 8 percent from 5 percent in 2014 tipped Japan into recession.

I give Prime Minister Abe credit for honesty. He openly admits that he wants more revenue to finance even bigger government.

All of which is sad since Japan used to be one of the world’s most market-oriented nations.

You also won’t be surprised to learn that the OECD is being a cheerleader for a higher VAT in Japan.

Speaking of which, let’s look at what a new OECD report says about value-added taxes.

VAT revenues have reached historically high levels in most countries… Between 2008 and 2015, the OECD average standard VAT rate increased by 1.5 percentage points, from 17.6% to a record level of 19.2%, accelerating a longer term rise in standard VAT rates… VAT rates were raised at least once in 23 countries between 2008 and 2018, and 12 countries now have a standard rate of at least 22%, against only six in 2008… Raising standard VAT rates was a common strategy for countries…as increasing VAT rates provides immediate revenue.

And here’s a chart from the study that tells you everything you need to know about how politicians behave once they have a new source of tax revenue.

Incidentally, there’s another part of the report that should be highlighted.

For all intents and purposes, the OECD admits that higher taxes are bad for growth and that class-warfare taxes are the most damaging method of taxation.

…increasing VAT rates…has generally been found to be less detrimental to economic growth than raising direct taxes.

What makes this excerpt amusing (at least to me) is that the bureaucrats obviously want readers to conclude that higher VAT burdens are okay. But by writing “less detrimental to growth,” they are admitting that all tax increases undermine prosperity and that “raising direct taxes” (i.e., levies that target the rich such as personal income tax) is the worst way to generate revenue.

Last but not least, I’ll recycle my video explaining why a VAT would be very bad news for the United States.

Everything that has happened since that video was released in 2009 underscores why it would be incredibly misguided to give Washington a big new source of tax revenue. And that’s true even if the people pushing a VAT have their hearts in the right place.

The only exception to my anti-VAT rigidity is if the 16th Amendment is repealed, and then replaced by something that unambiguously ensures that the income tax is permanently abolished. A nice goal, but I’m not holding my breath.

P.S. One of America’s most statist presidents, Richard Nixon, wanted a VAT. That’s a good reason for the rest of us to be opposed.

I never saw The Nightmare Before Christmas, a 1993 film. But that’s fine, because I am already dealing with my own nightmare with the holiday just around the corner.

We’ll start with this disconcerting report a couple of days ago from Politico.

Is the real lesson from tax reform that Americans rely too much on the income tax to fund their government? …Most other industrial nations lighten the load on their income tax by combining it with some form of consumption taxes… “If you want a code that is predictable and simple and competitive with rates on the global market place, you have to bring in other sources of income, other than the income tax,” said Sen. Ben Cardin (D-Md.). “A progressive consumption tax is the most logical way to move forward but we’re not there yet. I think ultimately we’ll get there.”

By the way, there’s a huge mistake in the above excerpt.

I don’t know if it’s because of dishonesty of incompetence, but the reporter is wrong to claim that other nations “lighten the load of their income tax.” Here’s a chart, based on OECD data, comparing the burden of personal income tax for the U.S. and Western Europe.

In other words, governments adopt VATs because politicians want to spend more.

And what sort of spending will we get?

Our statist friends are salivating at the thought of financing a bigger welfare state.

As a rule, the regressive nature of consumption taxes makes them less attractive to Democrats. But given concerns about climate change, a carbon tax is one consumption tax that has begun to attract some following. And economist Henry Aaron at the non-profit Brookings Institution said Democrats are “short-sighted” if they reject consumption taxes… Given the aging population and desire to do more to help workers adjust to technologies that threaten their jobs, the needs are there. “The bulk of redistribution occurs on the expenditure side of the budget,” Aaron said. “Those of us who want more progressivity would rather see a progressive tax … but the impact on income redistribution is going to be overwhelmed by what is done with revenue on the expenditure side. That’s going to completely overwhelm any regressivity in the collection mechanism.”

And here are some excerpts from a Yahoo column from earlier this month.

We’re being warned that politicians will use the next fiscal crisis to impose a VAT.

…at some point, the United States will have to reduce annual deficits that could swell to $1 trillion per year as early as 2019. Republicans would prefer to solve that problem by cutting social spending. But that seems unlikely. To make a difference, cuts in programs such as Social Security and Medicare would have to be vast, which would outrage voters. A more likely solution is a national consumption tax, otherwise known as a value-added tax, or VAT. “A 5% VAT would raise an enormous amount of money,” says Jeremy Scott, a tax attorney who is vice president of editorial at the publisher Tax Analysts. “The next major fiscal crisis might be followed by a VAT.”

Gee, isn’t that wonderful. The politicians will spend us into a fiscal cul-de-sac, and then use that spending crisis as an excuse to seize more of our money.

And I can’t resist sharing this passage to remind folks that those of us who opposed the “border-adjustment tax” were on the side of the angels. The BAT was basically a pre-VAT.

House Republicans actually proposed a tax similar to a VAT in the tax plan they introduced in 2016, and carried into 2017 as the starting point for the Trump tax cuts. That tax alone would have raised $1.2 trillion in new revenue during the first decade and more during the second decade — a large pot of new funds that would have allowed significant cuts elsewhere in the tax code. That tax was controversial, however, and Trump declared it too complicated. So House Republicans dropped it. Still, old ideas have a way of coming back around in Washington.

Yes, it is certainly the case that bad ideas never go away in Washington.

Let’s close with an amusing poem from Reddit‘s libertarian page.

I’m currently in Tokyo for an Innovation Summit. Perhaps because I once referred to Japan as a basket case, I’ve been asked to speak about policies that are needed to boost the nation’s competitiveness.

That sounds like an easy topic since I can simply explain that free markets and small government are the universal recipe for growth and prosperity.

But then I figured I should be more focused and look at some of Japan’s specific challenges. So I began to ponder whether I should talk about Japan’s high debt levels. Or perhaps the country’s repeated (and failed) attempts to stimulate the economy with Keynesianism. And Japan’s demographic crisis is also a very important issue.

But since I only have 20 minutes (not even counting Q&A), I don’t really have time for a detailed examination on any of those topics. So I was still uncertain of how best to illustrate the need for pro-market reforms.

My job suddenly got a lot easier, though, because Eduardo Porter of the New York Times wrote a column today that includes a graph very effectively illustrating why Japan is in trouble. Simply stated, the country is on a very bad trajectory of ever-higher taxes.

To elaborate, Japan used to have a relatively modest tax burden, as least compared to other industrialized nations. But then, thanks in part to the enactment of a value-added tax, the aggregate tax burden began to climb. It has jumped from about 18 percent of economic output in 1965 to about 32 percent of gross domestic product in 2015.

By the way, I feel compelled to digress and point out that Mr. Porter’s column was not designed to warn about rising taxes in Japan. Instead, he was whining about non-rising taxes in the United States. I’m not joking.

American tax policy must stand as one of the great mysteries of the global political economy. In 1969…federal, state and local governments in the United States raised about the same in taxes, as a share of the economy, as the government of the average industrialized country: 26.6 percent of gross domestic product, against 27 percent among the nations in the Organization for Economic Cooperation and Development. Nearly 50 years later, the tax picture has changed little in the United States. By 2015, …the figure was 26.4 percent of G.D.P. But across the market democracies of the O.E.C.D., the share had climbed by an average of more than seven percentage points. …Americans are paying dearly as a result, as their comparatively small government has proved incapable of providing an adequate safety net…there is no credible evidence that countries with higher tax rates necessarily grow less.

Now that I got that off my chest, let’s get back to our discussion about Japan.

Looking at the data from Economic Freedom of the World, Japan ranked among the world’s 10-freest economies as recently as 1990. Today, it ranks #39. That is a very unfortunate development, though I should point out that the nation’s relative decline isn’t solely because of misguided fiscal policy.

I’ll close by noting that even the good news from Japan isn’t that good. Yes, the government did slight lower its corporate tax rate so it no longer has the highest burden among developed nations. But having the second-highest corporate tax rate is hardly something to cheer about.

P.S. Since today’s column looks at the most depressing Japanese chart, I should remind people that I shared the most depressing Danish PowerPoint slide back in 2015. I may need to create a collection.

P.P.S. I doubt anyone will be surprised to learn that the OECD and IMF have been encouraging bad policy for Japan.

P.P.P.S. If I had to guess, I would say that Japan’s government is probably more competent than average. But that doesn’t mean it’s incapable of some bone-headed policies, such as a regulatory regime for coffee enemas and a giveaway program that was so convoluted that no companies asked for the free money.

Needless to say, my comment about being “nice” was somewhat sarcastic. But I was making a serious point about the United States having a very “progressive” fiscal system. The top-20 percent basically pay for government and those in the bottom half are net recipients of that involuntary largesse.

I also pointed out a huge difference between the United States and Europe. Governments on the other side of the Atlantic impose much higher burdens on lower-income and middle-class taxpayers.

…the big difference between the United States and Europe is not taxes on the rich. We both impose similar tax burden on high-income taxpayers, though Europeans are more likely to collect revenue from the rich with higher income tax rates and the U.S. gets a greater share of revenue from upper-income taxpayers with double taxation on interest, dividends, and capital gains (we also have a very punitive corporate tax system, though it doesn’t collect that much revenue). The real difference between America and Europe is that America has a far lower tax burden on lower- and middle-income taxpayers. Tax rates in Europe, particularly the top rate, tend to take effect at much lower levels of income. European governments all levy onerous value-added taxes that raise costs for all consumers. Payroll tax burdens in many European nations are significantly higher than in the United States.

So do this mean European politician don’t like ordinary people?

I could make a snarky comment about the attitudes of the political elite, but I’ll resist that temptation and instead point out that taxes in Europe are much higher for the simple reason that government is much bigger and that means some segment of the population has to surrender more of its income.

But here’s the $64,000 question that we want to investigate today: Why are European governments pillaging lower-income and middle-class taxpayers instead of going after the “evil rich” and “greedy corporations”?

Part of the answer is that there aren’t enough rich people to finance big government. But the most important factor is the Laffer Curve. Politicians can impose higher tax rates on upper-income taxpayers and companies, but that doesn’t necessarily translate into higher revenue. Simply stated, well-to-do taxpayers have considerable ability to earn less income and/or report less income when tax burdens increase, and they do the opposite when tax burdens decrease.

So even if politicians want to fleece upper-income taxpayers, that’s not a successful method of generating a lot of revenue.

Which is why a shift from a medium-sized welfare state (such as what exists in the United States) to a large-sized welfare state (common in Europe) means huge tax increases on ordinary taxpayers.

And here are three charts from the new study that tell a very persuasive story (and a depressing story for ordinary taxpayers).

First, we can see how the average tax burden has increased substantially over the past 50 years.

And who is paying all that additional money to politicians?

As you can see from this second chart, income tax revenues have become a less-important source of revenue over time while social insurance taxes (mostly paid by lower-income and middle-class taxpayers) have become a more-important source of revenue.

The third chart shows the evolution of the value-added tax burden. This levy takes a big bite out of the paychecks of ordinary people and the rate keeps climbing over time (and if we looked just at European governments that are part of the OECD, the numbers are even more depressing).

Now let’s put this data in context.

The United States now has a medium-sized welfare state financed mostly by upper-income taxpayers.

And if we leave policy on auto-pilot and there’s a substantial increase in the burden of government spending, it’s simply a matter of time before politicians figure out new ways of taking more money from lower-income and middle-class taxpayers.

Yes, they may also impose higher rates on “rich” taxpayers, but that will be mostly for symbolic purposes since those levies won’t generate substantial revenue.

Whenever I see an otherwise sensible person express support for a value-added tax, it triggers a Pavlovian response. And it’s not a favorable reaction.

So what happened? Have I surrendered to big government? Did I ingest some magic mushrooms?

Actually, I think you’ll agree that I’m still the same lovable guy. Yes, Professor John Cochrane of the University of Chicago (also a Cato adjunct scholar) has a column in the Wall Street Journal that embraces a VAT. But unlike all of the others I just cited, he includes a condition that is mandatory, necessary, vital, and non-negotiable. It’s so important that it deserves the opposite of fine-print treatment.

…eliminate entirely the personal and corporate income tax, estate tax and all other federal taxes. …it is essential that the VAT replace rather than add to the current tax system, as it does in Europe.

Amen. John hits the nail on the head.

The VAT isn’t theoretically bad. Like the flat tax, it would have one rate. There also would be no double taxation of saving and investment. And it also can be designed to have no loopholes.

In other words, the good news is that the VAT – when compared to the internal revenue code – is a less-destructive way of generating revenue.

The bad news, though, is that the VAT is capable of generating a lot of revenue. And as we’ve seen in Europe, that’s a recipe for enabling a larger burden of government spending.

Which is why the idea of a VAT should only be on the table if the plan would first abolish all other federal taxes. Which is what John is proposing.

Except I’d take it one step farther. Just like I’ve argued when contemplating a national sales tax, I’d only allow the VAT if we first repeal the 16th Amendment and replace it with something so ironclad that even John Roberts and Ruth Bader Ginsberg couldn’t rule in favor of an income tax at some point in the future.

By the way, John is right that the economy would grow faster if the income tax was totally abolished. The current system is filled with warts.

Much of the current tax mess results from taxing income. Once the government taxes income, it must tax corporate income or people would incorporate to avoid paying taxes. Yet the right corporate tax rate is zero. Every cent of corporate tax comes from people via higher prices, lower wages, or lower payments to shareholders. And a corporate tax produces an army of lawyers and lobbyists demanding exemptions. An income tax also leads to taxes on capital income. Capital income taxes discourage saving and investment. But the government is forced to tax capital income because otherwise people can hide wages… The estate tax can take close to half a marginal dollar of wealth. This creates a strong incentive to blow the family money on a round-the-world cruise, to spend lavishly on lawyers, or to invest inefficiently to avoid the tax. …A reformed tax code should involve no deductions—including the holy trinity of mortgage interest, employer-provided health insurance, and charitable deductions. The interest groups for each of these deductions are strong. But if the government doesn’t tax income in the first place, these deductions vanish without a fight.

By the way, I will quibble with a couple of things he wrote.

First, I don’t necessarily think the correct corporate tax rate is zero. What’s important is eliminating either the corporate tax or the tax on dividends. That way the income is only taxed once. And since it’s probably administratively easier to tax the income once at the business level rather than once at the shareholder level, I’m not fixated on abolishing the corporate tax.

Third, he should have explicitly included the state and local tax deduction in his list of loopholes to abolish (I’m guessing he assumed it would be the first deduction on the chopping block and therefore didn’t need to be mentioned).

There’s another part of John’s column that deserves attention. He points out that you need to have small government if you want a low tax burden.

…if the federal government is going to spend 20% of gross domestic product, the VAT will sooner or later have to be about 20%. Tax reform is stymied because politicians mix arguments over the rates with arguments over the structure of taxes. This is a mistake. They should first agree to fix the structure of the tax code, and later argue about rates—and the spending those rates must support.

At the risk of being pedantic, I think the VAT rate would have to be significantly above 20 percent, both because the tax base will be smaller than GDP and also because there will be loopholes or rebates. But the point he’s making is spot on. You can’t have a low tax rate and a big government. I’ve made the same point when writing about Belgium and Germany, nations where middle-class taxpayers are pillaged because the welfare state is too big.

My bottom line on this issue is that Professor Cochrane has produced a column showing that a VAT is theoretically worth considering, but only if all other federal taxes are permanently abolished.

As I’ve written before, our fight to restrain the size and scope of government will be severely hamstrung – perhaps even mortally wounded – if the crowd in Washington ever succeeds in getting a value-added tax as a new source of revenue.

But what makes this battle especially frustrating is that there are some otherwise sensible people who are on the wrong side of the issue. I was stunned, for instance, when Rand Paul and Ted Cruz included VATs as part of their presidential tax plans.

In a column for the Washington Times, Professor Peter Morici argues for a VAT instead of the income tax.

The current system imposes terribly high rates and a myriad of special-interest credits and deductions. It requires expensive record keeping that drives taxpayers mad and complex auditing functions at the Internal Revenue Service that have proven susceptible to political abuse… The most effective reform would be to simply junk the personal and corporate income taxes in favor of a VAT. The Treasury annually collects about $2 trillion through personal and corporate taxes. This could be replaced by an 11 percent national sales tax on all private purchases and payments.

This is good in theory, but it’s a high-risk fantasy. The politicians in DC who want a VAT are not proposing to get rid of other taxes. Instead, they want the VAT in addition to income taxes.

So unless Morici has some plan to fully repeal income taxes (and to amend the Constitution to prohibit income taxes from being imposed in the future), his support for a VAT plays into the hands of those who want a new levy to finance bigger government (which is exactly what happened in Europe).

Even more troubling, he confirms my fears that the border-adjustable tax serves as a stalking horse for a VAT.

Several House Republicans, led by Ways and Means Chairman Kevin Brady, propose to do essentially this for the corporate but not the personal income tax. …This proposal has…flaws. …The answer is simple — generalize Mr. Brady’s reforms to include the personal income tax as well. Junk it and impose a VAT of 11 percent on all economic activities.

Foreign governments rely more on value-added taxes (VAT), which approximates a national sales tax. Those are rebatable on exports and applied to imports under World Trade Organization rules… This places U.S.-based businesses at a competitive disadvantage.

Now let’s look at another column with a misguided message. Writing for The Hill, Jim Carter of Emerson and former Congressman Geoff Davis argue for a VAT.

…enact a payroll tax holiday similar to the one Americans enjoyed in 2011 and 2012. Only this time the tax holiday would be permanent. …How can the government make up for the revenue lost from the payroll tax cut? One idea: eliminate the deduction that businesses get for the wages and benefits they pay their employees. …this would generate a massive $11.6 trillion in revenue over 10 years.

Call me crazy, but I get very nervous about plans that generate “massive…revenue” for Washington. Especially when the plan proposed by Carter and Davis is actually a subtraction-method VAT.

And just like Morici, they think the House Better Way Plan paves the way for that pernicious levy.

Abolishing labor deductibility also generates enough revenue to lower the tax rates on business income five percentage points below the rates envisioned by the House Republican “blueprint” for tax reform… Add the House blueprint’s other provisions…this modified House blueprint would be roughly revenue-neutral.

Moreover, Carter and Davis don’t even pretend that the income tax might be abolished. They prefer instead to go after the payroll tax, which is far less damaging.

Moreover, they want to add other statist policies to their VAT scheme.

Add President Trump’s childcare proposals and a Republican commitment to link tax reform to additional infrastructure funding, and congressional Democrats would have little excuse not to work with Republicans.

Now let’s look at a Washington Postcolumn by Alan Murray.

…in tax policy, as in health-care policy, the United States is notoriously ineffective and inefficient. As the world’s richest nation, the United States has more capacity to tax than any other country. But…we rank near the bottom of industrialized nations in our effectiveness at doing so. …Reid…devotes a chapter to the value-added tax, which he calls “the most successful taxation innovation of the last sixty years.” …it turns out to be relatively easy to enforce. …Reid quotes former Federal Reserve chairman Alan Greenspan saying a VAT is the “least worst” way to raise taxes. “It has been adopted in every major nation on earth and in most small nations as well,” he says.

Yes, you read correctly. He’s grousing that the federal government isn’t demonstrating “effectiveness” when it comes to maximizing its “capacity to tax.”

For what it’s worth, I’m grateful that America hasn’t copied Europe by trying to squeeze every possible penny from taxpayers. And I’m specifically thankful that we haven’t copied them by imposing a VAT to finance bigger government.

I was amused by this passage in Murray’s column.

Critics of Reid’s plan, of course, won’t be hard to find. …Conservatives will attack the value-added tax as a money machine that leads to bigger government.

Of course supporters of limited government will make that complaint. That’s why statists want a VAT. Heck, Murray’s column openly states that the VAT would boost America’s “capacity to tax.”

For those who favor restraints on government, the last thing we want is a government that figures out ways to extract more revenue from the economy’s productive sector.

Let’s close by citing some research published last year.

Writing for the Wall Street Journal, Professor Ed Lazear of Stanford University warns that a VAT, even if part of an otherwise attractive tax plan, almost surely will lead to an increased burden of government spending.

…keeping a value-added tax low and substituting it for other more-regressive taxes has proven almost impossible. All 34 countries in the Organization for Economic Cooperation and Development, except the U.S., have a VAT. …26 countries have higher VATs now than they did when they first instituted the tax. …The U.K., Italy and Denmark have all raised their VATs by 10 percentage points or more. The VAT, wherever it has been implemented, has been a money machine for big government.

What about the notion that VATs simply replace other taxes?

Unfortunately, that’s not the case.

…for every 1 percentage point that the VAT increases, the tax burden rises by about 0.8 of a percentage point. Were it a pure substitute tax, raising the VAT would have no effect on total taxes collected because other taxes would be reduced by a corresponding amount. Unfortunately, that hardly ever happens. …America may be headed toward a European-style VAT tax and ever-larger government.

Prof. Lazear has some additional data posted at the Hoover Institution website. Here’s a chart that should frighten every fiscally responsible person.

And don’t forget the chart I shared showing how the VAT has jumped significantly in Europe in the past few years.

To conclude, here’s my video on why the value-added tax is so dangerous to good fiscal policy.

P.S. You can enjoy some amusing – but also painfully accurate – cartoons about the VAT by clicking here and here.

My crusade against the border-adjustable tax (BAT) continues.

In a column co-authored with Veronique de Rugy of Mercatus, I explain in today’s Wall Street Journal why Republicans should drop this prospective source of new tax revenue.

…this should be an opportune time for major tax cuts to boost American growth and competitiveness. But much of the reform energy is being dissipated in a counterproductive fight over the “border adjustment” tax proposed by House Republicans. …Republican tax plans normally receive overwhelming support from the business community. But the border-adjustment tax has created deep divisions. Proponents claim border adjustability is not protectionist because it would automatically push up the value of the dollar, neutralizing the effect on trade. Importers don’t have much faith in this theory and oppose the GOP plan.

Much of the column is designed to debunk the absurd notion that a BAT is needed to offset some mythical advantage that other nations supposedly enjoy because of their value-added taxes.

Here’s what supporters claim.

Proponents of the border-adjustment tax also are using a dodgy sales pitch, saying that their plan will get rid of a “Made in America Tax.” The claim is that VATs give foreign companies an advantage. Say a German company exports a product to the U.S. It doesn’t pay the American corporate income tax, and it receives a rebate on its German VAT payments. But an American company exporting to Germany has to pay both—it’s subject to the U.S. corporate income tax and then pays the German VAT on the product when it is sold.

Sounds persuasive, at least until you look at both sides of the equation.

When the German company sells to customers in the U.S., it is subject to the German corporate income tax. The competing American firm selling domestically pays the U.S. corporate income tax. Neither is hit with a VAT. In other words, a level playing field.