Google and Meta CEOs both out in last 24 hours now agreeing with my AI Arms Race narrative.

There are 4 major players in this game theory problem, and two are now on-the-record about their strategies.

Since starting at @sequoia, I've been reflecting on the massive CapEx buildout in AI.

For today's GPUs to payback, $200B of revenue will need to be generated per year of CapEx.

Long-term, this is good for startups. Short-term, it could get messy.

With Character dropping out, the qualifying round of the AI race is now officially over.

Congrats to the finalists: Microsoft/OpenAI, Amazon/Microsoft, Google, Meta and xAI.

The next phase begins: One defined more by the construction worker than the research scientist.

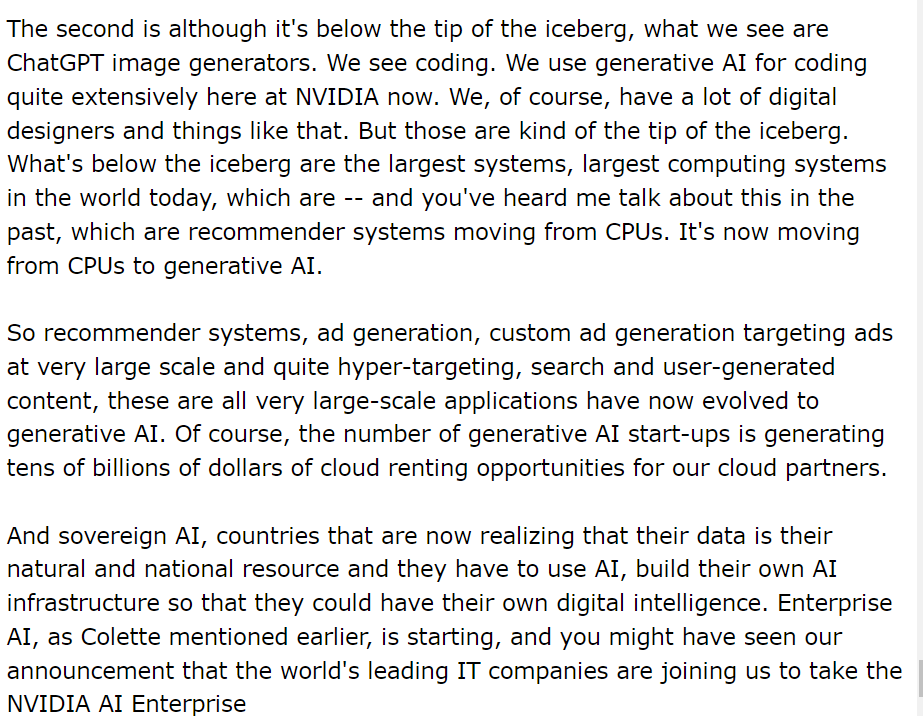

NVDA was asked our $600B question on Q2 call: Where is the customer's customer's revenue?

Their answer:

1. Traditional workloads will move from CPU to GPU

2. ChatGPT and coding AI

3. Meta saves $ using GPUs for algos

4. Countries buying GPUs

Is this enough to justify the hype?

Bootstrapped to $1M ARR with 4 people. Now: $10M ARR, 2,500+ customers.

Juicebox is more than a tool, it’s a new way of recruiting. Proud to back @davepaffenholz and @ishangpta—their grit & hustle is next-level.

Excited to announce Juicebox has raised $36M in funding, including our Series A led by Sequoia Capital (@sequoia) - to help the world’s leading teams win the talent war.

More below 🧵

Nvidia just became the most valuable company in the world.

In September, I published AI’s $200B Question.

The question I had then was: “Where is all the AI revenue?

Below is an update on what’s changed & what hasn’t:

AI labs are starting to look like pro sports teams.

Backed by deep-pocketed owners.

Star players making 8-figure packages.

Fierce, fluid battles for top talent

New “draft class" each year

Why talent — not compute — is now the AI bottleneck:

Morning after last night's "AI Super Bowl."

Here's where we stand on AI's $600B question:

(1 & 2) Nvidia: CPU to GPU

(3 & 4) Meta: AI game theory

(5 & 6) Google: Underinvesting vs. overinvesting

(7 & 8) Microsoft: M365 & Github copilots

(9 & 10) Amazon: Data center logistics

Excited to share our launch of Kela Defense from stealth today, including a great profile in the @WSJ.

As my first Sequoia investment, this company has been a huge focus for me over the last year. We’re excited to finally share what we’ve been working on.

New post: AI CapEx Now Hinges on Deus ex machina

With talk of 100 GW or 250 GW of energy buildout, a really big plot twist would be needed to make the math pencil out.

Nothing short of AGI will be enough to justify the investments now being proposed for the coming decade.

Here’s the question now being asked all across the AI ecosystem: Is there a way for someone else to take on the demand risk from AI, while I capture the profits? (1/3)

New Post: Circular Deals & Supply Chain Dynamics

1/ The big story of 2025 has been the direct transfer of data center demand risk from hyperscalers to NeoClouds and chip companies ("the demand hot potato"). Circular deals crystallize this dynamic.

The next big catalyst in AI is the launch of 100k clusters. Everyone has committed to this path.

If scaling laws hold at 100k, we'll get another leg of CapEx. If not, things will slow down.

Given physical requirements, this is ~1+ years away. We may be in limbo for a while.

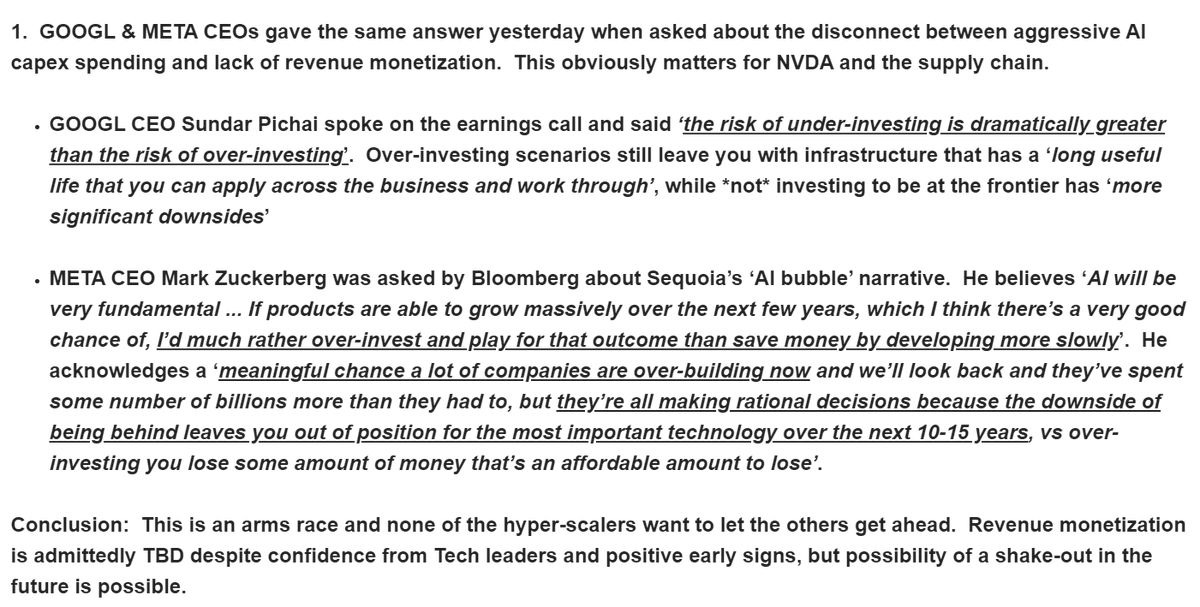

Big day in the market. Zuck & Sundar acknowledged how much AI CapEx is FOMO vs. actual revenue. Public market grappling with updating their AI narrative.

Full breakdown here: