The analysis and conclusions set forth are those of the authors and do not indicate concurrence by other members of the research staff or the Board of Governors

Higher inflation can lead to greater efficiency. It all has to do with the price dispersion that inflation generates, which might motivate some consumers to search for the lowest prices, increasing competition among sellers. federalreserve.gov/econres/feds/i…#FEDSPaper

Research shows recent tariffs associated with reductions in manufacturing employment: a positive effect from lower import competition offset by negative effects from rising input costs & retaliatory tariffs. Tariffs also lead to higher factory-gate prices. go.usa.gov/xpHw5

Decline in interest and tax expenses is responsible for a full 1/3 of all corporate profit growth over the prior 2 decades. This boost is unlikely to continue, indicating notably lower profit growth, and thus stock returns, in the future: federalreserve.gov/econres/notes/…#FedResearch

Who's driving consumer spending? It's middle- and high-income households! They're the ones fueling strong spending growth on retail goods and food services, while spending by low-income households has been flat. See this new #FEDSNote for more information:

New #FEDSPaper: The authors build a new measure of credit and financial market sentiment from Twitter data. They find that the Twitter Financial Sentiment Index (TFSI) helps predict intraday stock market returns. (1/2) federalreserve.gov/econres/feds/m…#EconTwitter

Welcome to the official Twitter research account of the @federalreserve. @FedResearch highlights new research in the Board’s working papers & notes series, staff articles, & conferences. In Dec, we will also tweet research published in Nov. go.usa.gov/xpGyc#EconTwitter

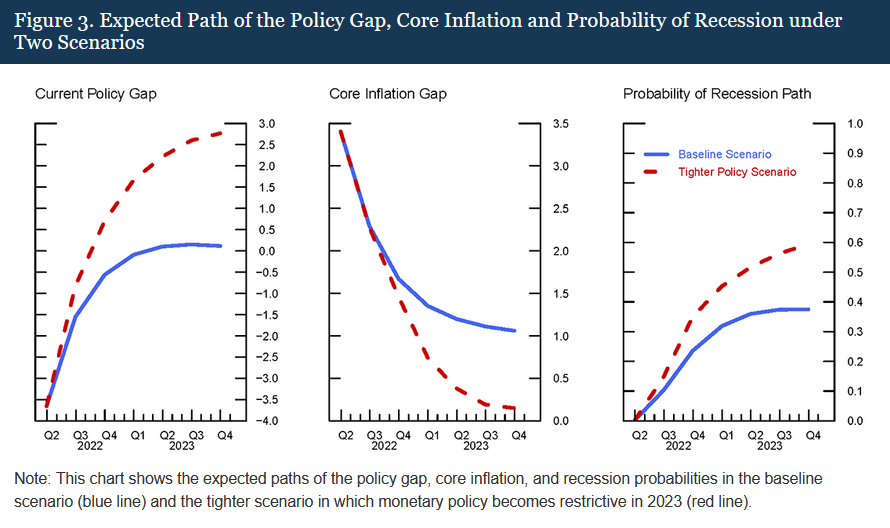

The path of inflation since the beginning of COVID has been historically and objectively difficult to predict. U.S. and foreign inflation uncertainty may be acting as a headwind to U.S. growth and pose challenges for monetary policy.

Inflation targeting has become the predominant monetary policy strategy and has been remarkably successful in anchoring inflation, reflecting its reaction process, which allows it to flexibly incorporate a wide range of factors. federalreserve.gov/econres/feds/t…#FEDSPaper#EconTwitter

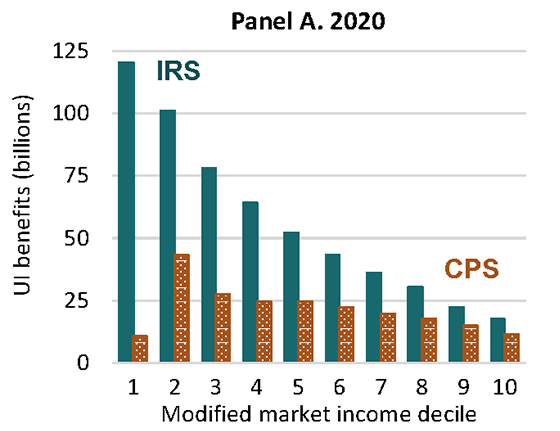

New #FEDSNote shows Census data understated the increase in unemp. benefits in 2020 - particularly among low-income families. As a result, official poverty rates were overstated by about 2 pct. points, and corrected poverty reached a 6-decade low: federalreserve.gov/econres/notes/…