So, it is official!

Yesterday Second Lane was publicly announced at Consensus 2023 in Austin, TX.

dApp functionality will be open to the public shortly.

Stay tuned

📢We’re excited to announce our partnership with @0G_labs Labs, supporting their highly anticipated AI Alignment Node Sale, launching on November 11, 2024. This sale marks a crucial step in building a safer, decentralized AI infrastructure that keeps AI systems honest and

Web 3 secondary market report, July 2023 - by SecondLane, 1

- $175m in Asks and Bids - a 47% increase in volume

- $2.6m avg offered amount vs $2.2m avg in June

- top projects: Worldcoin, Scroll, EigenLayer, Celestia, zkSync, Fuel, Starkware, LayerZero, Animoca, Aleo

Web 3 secondary market report, February 2024 - by SecondLane, 1

- $769M in deal volume (Asks and Bids) in February 2024

- $5M avg offered amount

- top projects: LayerZero, Solana, Fuel, Celestia, Fireblocks, Ronin, Mavia, Dymension, JTO, Pyth

Big respect to @Delphi_Digital and @3xliquidated for diving into this with us.

The report breaks down how secondaries are becoming a core part of digital asset infrastructure and factors driving this shift: evolving investor behavior, the pull of institutional capital, tighter

The digital asset secondary market is evolving.

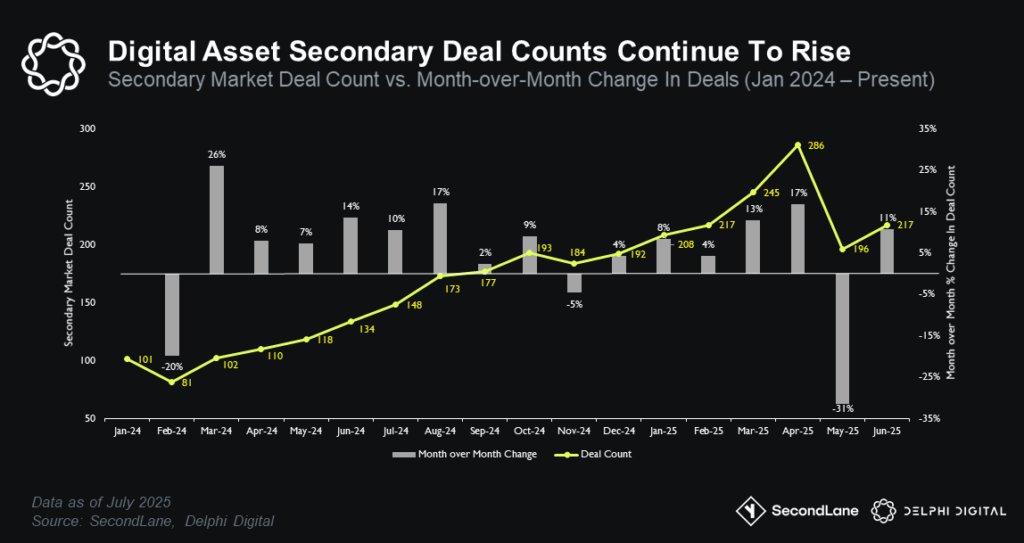

• Volumes surged 73% YoY to 413 deals as institutions flood in

• New tactical buyers now dominate compressing deal timelines

• Circle’s IPO sparked rotation into equity deals ahead of IPO wave

Read more here 👇

If we got a dollar every time our founder @Omar_Shakeeb said “transparency” on the latest @Unchained_pod, the SecondLane team could retire tomorrow. But we’re still here, building the private markets we want to see: transparent, compliant, accessible, and liquid.

🎧 Tune in:

📊 November Market Insights Are Out!

The secondary market hit $1.2B (+29%), driven by a 50% jump in SELL deal sizes and premiums soaring to ~95%.

Discounts held strong, with 70% of deals below last-round values, and liquidity was strongest in sectors like L1, L2, Privacy, and

In August, we observed a 10% rise in volume to the record $950M. The average offered amount slightly dipped by 8%, signaling a shift toward smaller deal sizes. Additionally, the premium-to-last-round FDV narrowed slightly, averaging 20% in August compared to 30% in July.

📊 September brought steady growth in the secondary market, with 264 offers (+2% from August) and a total order book value of $970M (up from $950M in August).

Buyer activity included 113 offers totaling $290M, up from $270M in August, with 70% listed at a discount. Sellers made