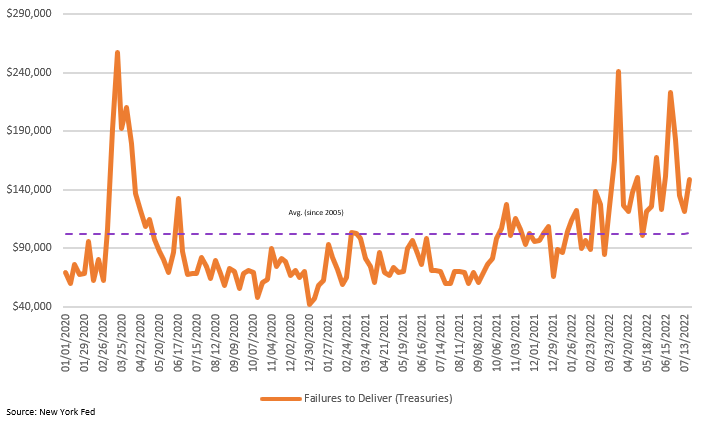

Liquidity is starting to deteriorate, and a great insight into this is the Repo market. Failures to deliver (Bonds used as collateral in Repurchase agreements) have been elevated and are up 22% on a WoW basis. This is a sign of liquidity event brewing.